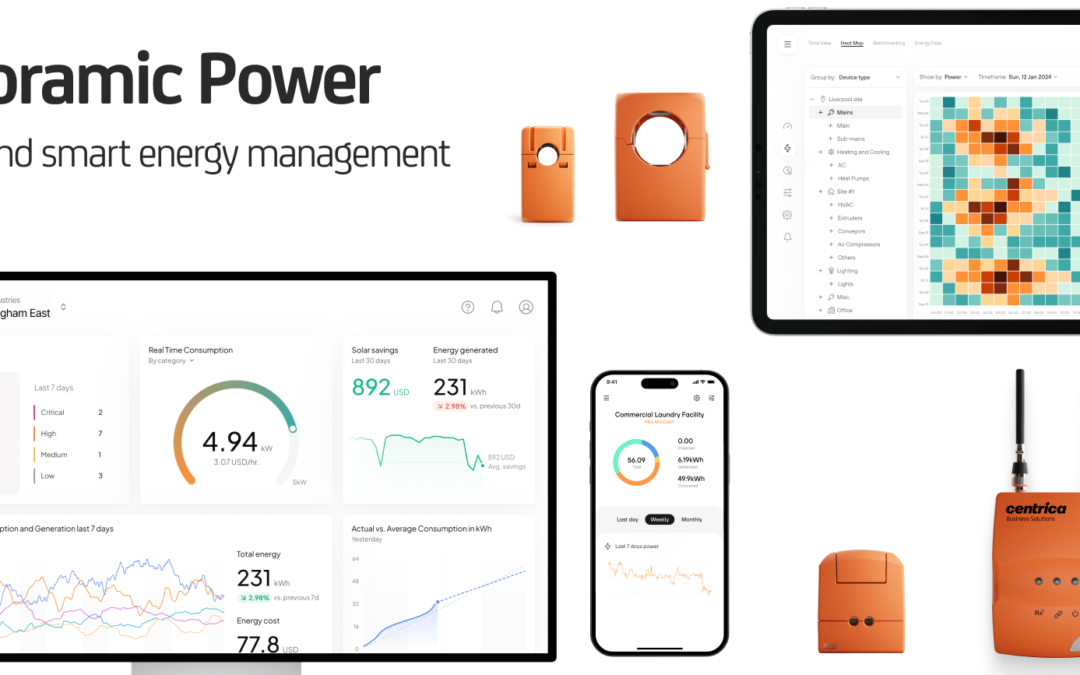

Smarter tools, deeper insights, better decision making — discover how Panoramic Optimise can transform your future of energy management.

Enhanced User Experience: Enjoy a sleek, intuitive design with quicker navigation and AI-driven quick search for improved results in seconds.

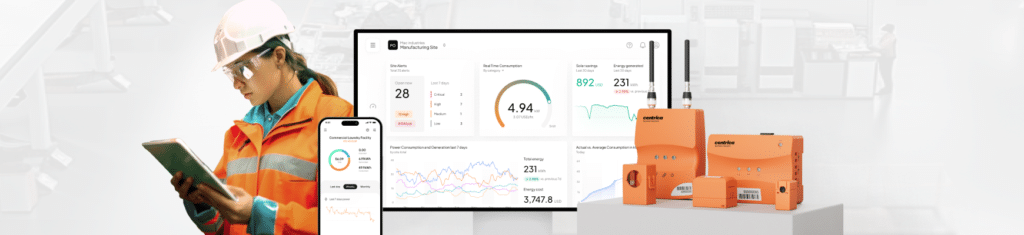

End-to-End Personalisation: Customise dashboards, widgets, device grouping, and naming. Tailor benchmarks, thresholds, and visualisations to your unique needs.

Continuous Innovation: Benefit from regular feature updates, cutting-edge improvements, and AI-powered features with a forward-looking roadmap.

Empowered Team Performance: Engage stakeholders across various departments with tools for teamwork, task delegation, and incident management.

Improved Performance and Security: Experience 80% faster load times, 50% fewer network errors, and top-tier data security on a robust cloud infrastructure.

Smarter Energy Intelligence: Gain deeper insights into energy patterns, custom benchmarks, and proactive maintenance with AI-powered tools tailored to your KPIs and workflows.

Smarter decisions with customisable widgets.

Multiple views, smarter insights, and deep data exploration.

Our expert team can help you unlock significant energy savings with a short-term return on investment (ROI). Typically, we can identify up to 25% savings with an ROI of less than 2 years.

We achieve this by conducting a comprehensive site-wide energy audit (Type 1), examining everything from lighting and HVAC systems to chillers, boilers, refrigeration and other energy-intensive systems. Additionally, we install Panoramic Power our non-intrusive energy intelligence system, providing real-time device-level energy data visibility. For more information check out a brief overview of our service here.

Has your organisation invested in commercial solar panels, or are you considering deploying solar power? If so, you might be looking for ways to maximise your return on investment (ROI).

In today’s challenging business environment, adapting your energy strategy is crucial. Objective tracking of your assets’ cost and performance is becoming increasingly important. Without this data, you could face additional pressure on your bottom line, complicating your budget amid rising costs.

The Power of Panoramic Power

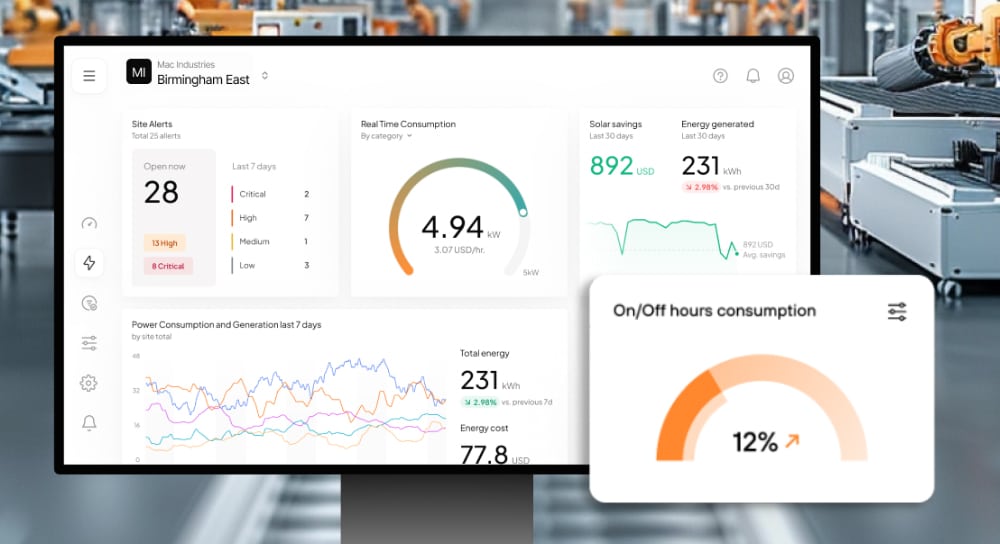

Panoramic Power’s end-to-end energy management and intelligence platform can help you clarify your energy picture. The benefits of real-time data start from the very beginning of your solar system’s lifetime. Panoramic Power can help you track your organisation’s electricity demand and energy costs. With real-time alerts and reporting, you’ll be able to view energy usage for your entire site. This can help you identify opportunities to cut wastage and reduce your total energy demand.

Lowering Usage and Reducing Costs

Lowering your energy usage means drawing less energy from the grid. This allows you to meet more of your total demand via your solar system, providing more stable prices and accurate forecasts. If you invested via capital sale, this could even help reduce your solar system’s payback period.

If you haven’t invested in solar power yet, tracking your energy usage can still benefit your business. Reduced usage means you’ll need a smaller system, with a 25% reduction resulting in a roughly 25% smaller solar system. This can lower your upfront costs and free up your budget for other investments.

Achieving Energy Efficiency

Energy efficiency is a priority for many organisations. For some, energy monitoring can deliver quick wins and effective short-term savings. However, progress can stall without a more granular view of energy usage and cost.

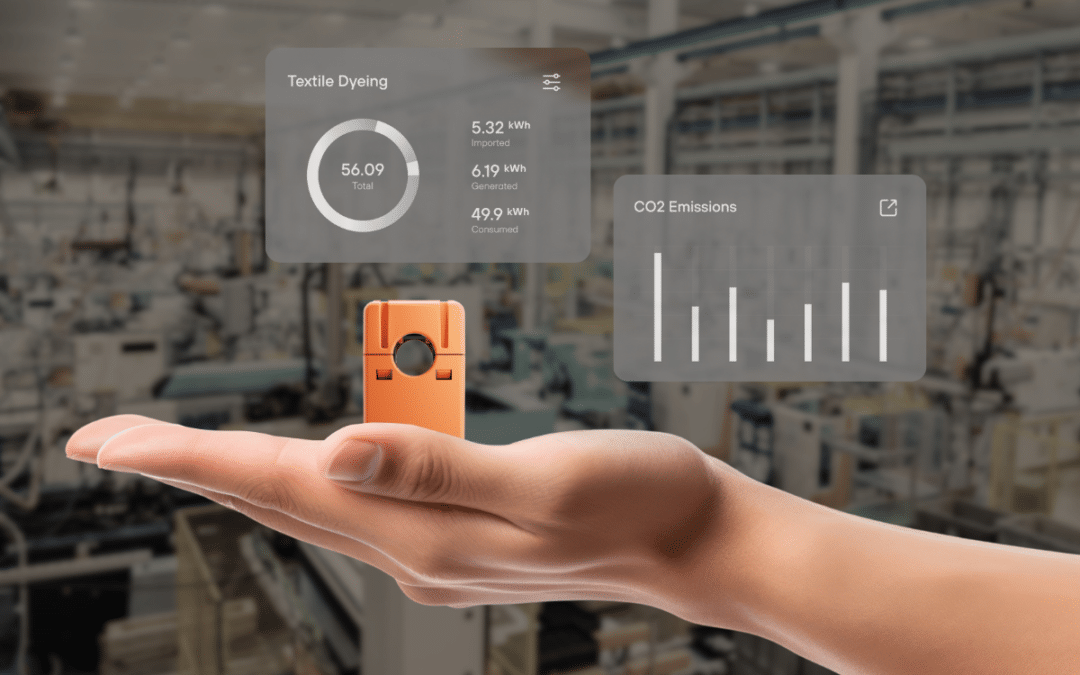

With device-level insights, you can track exactly how much energy you’re using and where. Panoramic Power provides a detailed view of where and when you could reduce your energy usage. By uncovering opportunities to cut back on wastage, you can ensure that you’re only using the energy you really need.

Transforming Your Energy Strategy

Pairing energy monitoring with commercial solar power can transform your energy strategy, offering dual benefits. Bringing your energy generation onsite reduces your reliance on grid supply, shielding you from volatile electricity prices. By tracking your energy demand, you’ll know you’re paying the right price for the right amount of electricity.

In conclusion, data-driven energy monitoring and insights can help you maximise your ROI in commercial solar power. By collecting, analysing, and acting on data-driven insights, you can bridge the gap between commitments and implementation, achieve your energy goals, and build a more sustainable future.

How Total Utilities Can Help

Our expert team can help you unlock significant energy savings with a short-term return on investment (ROI). Typically, we can identify up to 25% savings with an ROI of less than 2 years.

We offer the easiest-to-install, and fastest for ROI energy management solution, that scales effortlessly from a few devices to full-site or multi-site operations. Experience actionable insights and real-time analytics that drive efficiency and sustainability. Our solutions work for everyone, helping your organisation kickstart cultural transformation towards a sustainable future.

Total Utilities partners with Kristin School to provide real-time monitoring of solar panel performance with our world-class energy monitoring solution. Read their story here.

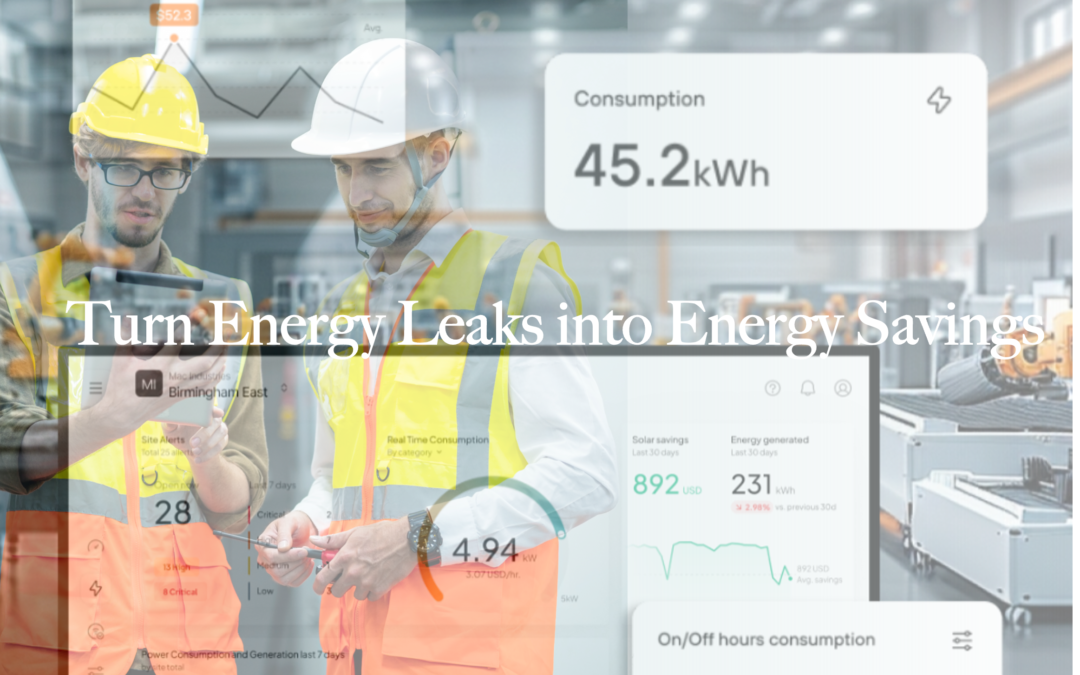

Hidden inefficiencies are draining your profits and hindering your sustainability goals.

We’re not talking about dramatic equipment failures that halt production. Instead, we’re exposing invisible efficiency killers—machines that appear fully operational while steadily eroding your bottom line and inflating your carbon emissions. The culprits are your most commonplace industrial machines: boilers, hot water systems, compressors, lighting, HVAC and refrigeration systems.

Every unit of wasted energy means lost money and unnecessary emissions. As New Zealand businesses face mounting pressure due to escalating energy prices, for executives tasked with controlling costs, Panoramic Power represents a transformative ally.

The Invisible Problem: Why Inefficiencies Go Unnoticed

Many inefficiencies remain hidden because you can’t fix what you can’t see. Machines that appear operational can quietly drain profits and inflate emissions. Without advanced energy monitoring, these “silent thieves” stay undetected, eroding both financial performance and sustainability credentials.

Total Utilities provides a simple, cost-effective way to identify quick wins and the real-time visibility needed to expose these invisible efficiency leaks, equipping businesses with actionable insights to transform waste into measurable gains.

Excessive Steam Discharge: Can account for up to 30% of energy waste.

Scale Buildup: A 1mm layer can increase fuel consumption by 2–5%.

Faulty Controls: Malfunctioning thermostats or regulators increase inefficiencies.

Real-life example: A Panoramic Power client identified that 30% of their steam was wasted. Real-time insights enabled targeted fixes, reducing gas usage and emissions.

Sediment Accumulation: Reduces heat transfer, requiring more energy.

Corrosion and Leaks: Often unnoticed until damage is extensive.

Real-life example: Monitoring revealed a pump running four times faster than needed. Adjustments led to significant energy and cost savings.

Compressed Air: The Hidden Energy Monster

Air Leaks: Drain 20–30% of output.

Short-Cycling: Misaligned systems disrupt efficiency.

Improper Pressure Settings: Cause waste and operational disruptions.

Real-life example: A bottling plant reduced compressor pressure from 100 PSI to 96 PSI, saving energy and reducing wear without affecting production.

HVAC Systems: The Silent Energy Drainers

Unbalanced Airflow: Causes some areas to overheat or over cool, wasting energy.

Dirty Filters: Reduce efficiency and increase energy consumption.

Faulty Thermostats: Lead to inconsistent temperatures and energy waste.

Real-life example: A client discovered that their HVAC system ran 24/7 due to a faulty thermostat. Fixing it saved significant energy and reduced costs.

Lighting Systems: The Overlooked Energy Consumers

Outdated Bulbs: Older lighting technology consumes more energy.

Improper Scheduling: Lights left on when not needed.

Inefficient Fixtures: Poorly designed fixtures waste light and energy.

Real-life example: A warehouse switched to LED lighting and implemented motion sensors, cutting their lighting energy use by 40%.

Refrigeration Units: The Hidden Cold Costs

Door Seals: Worn seals allow cold air to escape, increasing energy use.

Defrost Cycles: Inefficient cycles waste energy.

Temperature Settings: Incorrect settings lead to higher energy consumption.

Real-life example: A food processing plant adjusted its defrost cycles and repaired door seals, resulting in a 15% reduction in energy use.

Total Utilities leverages Panoramic Power to turn hidden inefficiencies into measurable improvements. Using real-time monitoring, predictive analytics, and customised dashboards, the platform:

Identifies inefficiencies across machines and systems.

Provides actionable insights to reduce energy waste.

This integration of visibility and intelligence empowers manufacturers to cut costs, lower emissions, and enhance competitiveness.

Why Panoramic Power Stands Out

Unlike generic energy monitoring tools, Panoramic Power aligns with executive priorities by translating data into strategic opportunities. The platform simplifies:

Inefficiency detection: Identify hidden energy drains.

Data customisation: Tailor dashboards to operational needs.

By addressing both cost savings and environmental impact, Panoramic Power helps users achieve measurable results and lead in sustainable innovation.

How Total Utilities Can Help

Our expert team can help you unlock significant energy savings with a short-term return on investment (ROI). Typically, we can identify up to 25% savings with an ROI of less than 2 years.

We achieve this by conducting a comprehensive site-wide energy audit (Type 1), examining everything from lighting and HVAC systems to chillers, boilers, refrigeration and other energy-intensive systems. Additionally, we install Panoramic Power our non-intrusive energy intelligence system, providing real-time device-level energy data visibility. For more information check out a brief overview of our service here.

Ready to start saving? Contact us today to schedule your energy audit and begin your journey towards greater efficiency and cost savings!

In today’s business landscape, whether your priority is energy efficiency, cost reduction, or sustainability, a successful long-term strategy relies on a degree of certainty about the future. When market conditions are volatile, a rigorous approach to data becomes more crucial than ever. Long-term uncertainty makes it challenging to plan and even harder to sell sustainability strategies within the wider business. However, a data-driven approach provides businesses with something tangible to build on.

The Role of Data and Analytics

For those looking to manage energy more effectively, data and analytics often focus on consumption, carbon emissions, and cost. Establishing baselines for all data sets and systematically tracking them as you make operational changes or implement new technologies is essential. This approach ensures you know what’s working, what isn’t, and why.

Addressing Energy Costs in New Zealand

With increasing pressure to control energy costs due to systemic market constraints in New Zealand, businesses must find ways to reduce energy usage. Simply absorbing costs is not a viable option. Understanding where your energy is going is crucial. By identifying operational inefficiencies, you can discover where savings can be made, helping you make smarter decisions.

Leveraging Real-Time Energy Intelligence

Combining self-powered, wireless sensors with real-time energy intelligence software provides the overview you need and allows you to analyse data to develop a data-driven strategy for the future. This approach can help mitigate costly downtime, reduce waste, enhance agility, and boost productivity.

Benefits Across Various Industries

Using end-to-end energy management tools to build energy intelligence offers benefits for various industries, types of operations, and facilities:

Industrial Manufacturers: Avoid equipment downtime by predicting failures, maximise energy savings, detect operational inefficiencies, and optimise overall equipment effectiveness. Typical results include reducing maintenance costs by 60%, equipment downtime by 50%, and equipment capital investment by 3-5% by extending the useful life of machinery.

Multi-Site Retail and Grocery Stores: Cut costs by reducing energy waste, optimise equipment and maintenance, enhance brand reputation through sustainability, and monitor the entire operation from one dashboard. Typical results include eliminating 30% excess energy consumption and a 10% reduction in energy costs, boosting net profit margins by up to 16%.

Commercial Buildings and Business Campuses: Predict failures and operational anomalies through real-time alerts, reduce energy waste, measure retrofit effectiveness, and continuously improve operational effectiveness. Typical results include cutting equipment maintenance costs by 40% and extending equipment lifetimes.

Panoramic Power: Your All-in-One Energy Intelligence Solution

Our expert team can help you unlock significant energy savings with a short-term return on investment (ROI). Typically, we can identify up to 25% savings with an ROI of less than 2 years.

We offer the easiest-to-install, and fastest for ROI energy management solution, that scales effortlessly from a few devices to full-site or multi-site operations. Experience actionable insights and real-time analytics that drive efficiency and sustainability. Our solutions work for everyone, helping your organisation kickstart cultural transformation towards a sustainable future.

Reducing waste costs is a crucial goal for many businesses. And the good news is, you don’t have to wait until your waste contract ends to reduce costs. Here are some effective strategies to help achieve this:

Conduct Waste Audits: Regularly analyse your waste streams to identify areas where waste can be minimised. This helps set reduction targets and track progress

Implement Recycling and Composting Programs: Incorporate recycling and composting practices into your daily operations. This reduces the amount of waste sent to landfills and can lower disposal costs

Reduce Packaging Waste: Choose products with minimal and recyclable packaging. This prevents waste from being created in the first place and can significantly cut costs

Switch to Reusable Products: Use reusable bags, bottles, containers, and other products to prevent waste from disposables. This not only reduces waste but also saves money in the long run

Optimise Processes: Focus on minimizing resource usage, such as energy, water, and raw materials, by optimising processes and adopting lean production methods

Promote Reuse: Encourage the reuse of materials, equipment, and packaging within your operations. This can reduce the need for new purchases and lower waste generation

Engage Employees: Educate and engage employees in waste reduction efforts. A company-wide culture of sustainability can lead to more effective waste management practices

Invest in Technology: Consider technological advancements such as waste-to-energy systems and eco-friendly materials for more efficient waste management

Review and Refine Strategies: Continuously assess and refine your waste reduction strategies to adapt to evolving regulations and best practices

By implementing these strategies, businesses can not only reduce waste costs but also contribute to a more sustainable future.

How Total Utilities Can Help

In 2024, the team at Total Utilities successfully managed $13.7 million worth of Waste and Recycling tenders, achieving impressive savings of $3.5 million for our clients. These savings ranged from as high as 59% to an average of 26% and were made up of better contract terms as well as increased landfill diversion.