New Zealand’s gas market is entering a period of structural change. PwC’s 2026 Gas Supply and Demand Study, prepared for the Gas Industry Company, highlights a future where indigenous gas supply continues to decline, major fields reach end‑of‑life, and commercial and industrial (C&I) customers face increasing uncertainty.

For businesses that rely on gas for process heat, manufacturing, food production, or backup generation, the implications are significant — and planning ahead is essential.

The State of the Gas Market: Key Findings from the PwC Study

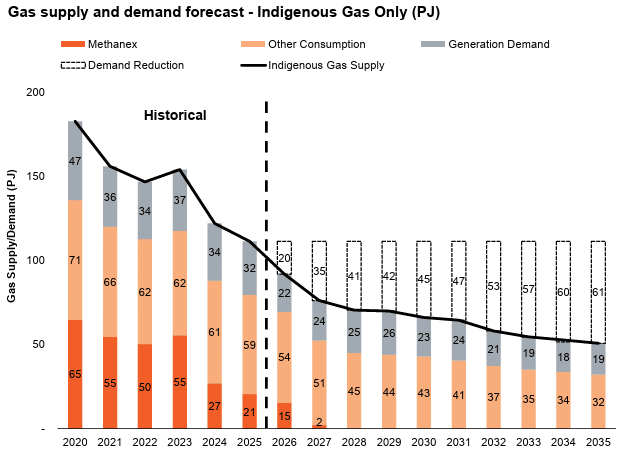

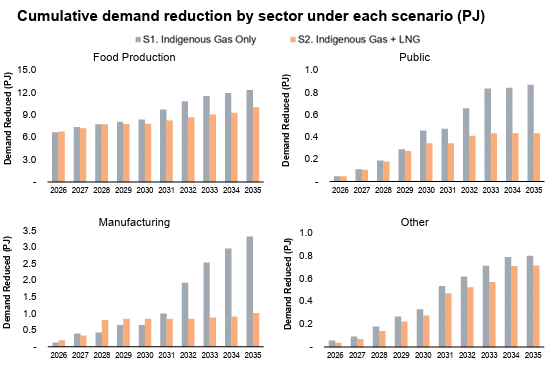

1. Domestic gas supply is declining faster than expected

New Zealand’s indigenous gas production has fallen to levels not seen in decades. Major fields are maturing, and by 2035 domestic supply could halve again. This creates structural scarcity and increases exposure to supply shocks.

2. Without LNG, the market becomes extremely tight

Gas demand must fall sharply by 2035

Industrial users face potential forced fuel switching

Electricity prices become more volatile, especially in dry years

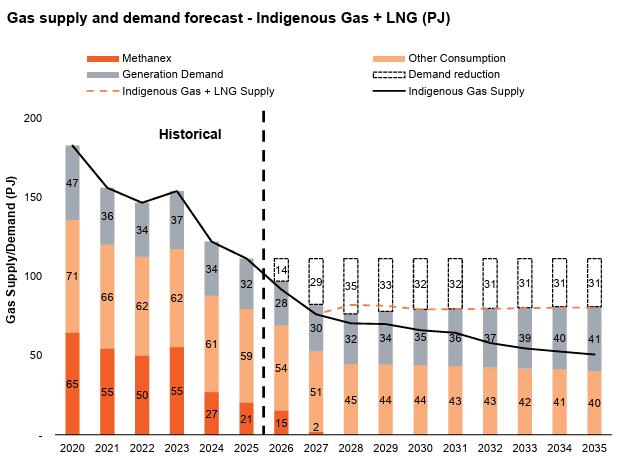

3. LNG imports from 2028 improve stability — but don’t eliminate risk

If LNG is introduced:

Prices become more stable

Electricity security improves

Industrial operations remain more viable

However, LNG still exposes New Zealand to global commodity markets, and the study makes it clear that significant electrification or alternative fuels will still be required from the late 2020s onward.

4. The 2030s will be a crunch period

Even with LNG, domestic supply continues to decline. Any delays in LNG infrastructure or new supply sources increase risk for C&I customers.

What This Means for Commercial & Industrial Energy Users

1. Expect higher and more volatile gas prices

Tight supply and declining production create upward pressure on pricing. Dry years will amplify volatility.

2. Contract availability will shrink

Retailers may:

Shorten pricing validity windows

Reduce willingness to quote

Prioritise large or strategic customers

Require longer‑term commitments

3. Forced switching is a real possibility

Industries relying on gas for process heat may face:

Mandatory curtailment

Loss of supply if fields decline faster than forecast

Higher costs if switching is unplanned

4. Decarbonisation pressure will intensify

Even with LNG, the study is clear: New Zealand must electrify or adopt alternative fuels at scale.

Key Recommendations for Total Utilities Clients

1. Secure long‑term gas contracts where possible

For businesses that must remain on gas in the medium term:

Lock in multi‑year supply agreements

Prioritise retailers with strong upstream positions

Consider hedging strategies

Avoid exposure to short‑term or spot‑driven pricing

2. Begin evaluating alternative fuels now

Depending on your process heat requirements, viable options include:

Electric boilers or industrial heat pumps

Biomass or wood pellets

Renewable LPG or bio‑LPG

Hydrogen‑ready equipment

Thermal storage solutions

3. Stress‑test your energy strategy

Consider:

What happens if gas supply is curtailed for 30–90 days

The impact of a dry‑year price spike

The risk of a retailer declining to renew your contract

The cost difference between proactive vs reactive fuel switching

4. Integrate energy security into long‑term planning

Businesses should incorporate:

Scenario modelling

Capex planning for alternative fuels

Electrification roadmaps

Carbon reduction pathways

Contingency planning for supply interruptions

How Total Utilities Can Help

1. Gas procurement and long‑term contract negotiation

We work with all major gas supplies, helping you secure competitive, reliable supply in a tightening market. Over the last few months we have been securing contracts of up to 5 years and while this does not guarantee gas supply, it does provide long term gas pricing security.

2. Ongoing market intelligence

We continuously monitor:

Gas supply conditions

Retailer behaviour

LNG developments

Electricity market dynamics

Policy and regulatory changes

3. Decarbonisation and feasibility studies

Our technical partners can assist your business build practical, staged plans that balance cost, operational requirements, carbon reduction, technology readiness, and risk management. From engineering assessments to procurement and implementation, they guide you through the entire transition process.

Final Thoughts

The PwC study is a clear signal: New Zealand’s gas market is tightening, and C&I customers must prepare for a future where gas is more expensive, less available, and increasingly uncertain.

Whether your business intends to stay on gas for the medium term or transition away from it, the decisions you make in the next 12–24 months will shape your resilience and competitiveness through the 2030s.

Total Utilities is here to help you navigate that journey with clarity, confidence, and data‑driven strategy.

A prominent educational institution in the Waikato operates a large campus with boarding facilities, relying heavily on natural gas for heating and hot water. Energy costs represent a significant portion of its operating budget, making cost control a priority.

The Challenge

As the school’s existing gas contract approached renewal, the incumbent supplier presented a renewal offer. While straightforward, the proposed rates were substantially higher than current market prices. Accepting the offer would have locked the school into two more years of inflated costs, putting pressure on budgets that could otherwise support educational programs.

The school needed:

A cost-effective solution without sacrificing service quality.

A smooth transition with minimal administrative burden.

Confidence that the new contract would remain competitive over time.

The Solution

Total Utilities conducted a comprehensive review of the school’s gas usage and current contract terms. Leveraging market expertise and supplier relationships, the team:

Benchmarked the incumbent’s renewal offer against competitive market rates.

Ran a competitive tender process with multiple suppliers.

Negotiated favorable terms and managed the transition seamlessly.

The Outcome

The new gas supply contract delivered $57,000 in savings over two years compared to the incumbent’s renewal offer. Additional benefits included:

Transparent pricing and improved contract terms

Budget certainty with locked-in competitive rates

Confidence in long-term cost control

Key Insights

Benchmarking renewal offers can uncover significant savings.

Competitive tendering drives better pricing and terms.

Expert procurement support ensures compliance and reduces risk.

“Total Utilities made the process simple and delivered real savings. Their expertise gave us confidence that we were getting the best deal.” – School Business Manager

How Total Utilities Can Help Your Business

Don’t let rising energy costs eat into your bottom line. At Total Utilities, we help Kiwi businesses lock in the most competitive natural gas rates available. Our expert team keeps an eye on market trends, negotiates on your behalf, and makes sure you get the best deal—saving you time and money.

Take control of your energy costs today.

👉 Get in touch with Total Utilities now and start optimising your natural gas pricing to future-proof your business.

Renée’s analysis goes beyond identifying problems. She’s actively advocating for change through two petitions aimed at reshaping New Zealand’s energy strategy and reforming the Emissions Trading Scheme (ETS).

🔑 Structural Reform

Renée argues that New Zealand’s government structure needs simplification. Overlapping and conflicting ministerial portfolios hinder long-term planning. She points to countries like Norway and Singapore as models of efficient governance and strategic foresight.

🔋 A Long-Term Energy Strategy

At the heart of her proposal is a 50-year bipartisan energy plan—one that balances traditional fuels with renewable innovation. Key elements include:

Continued use of coal, gas, LPG, diesel, and petrol where necessary for energy security and affordability.

Support for renewables like geothermal, solar, wind, biomass, and emerging technologies (e.g., hydrogen, biogas, small nuclear).

Infrastructure upgrades to support distributed generation and grid stability.

Regular reviews to adapt to evolving technologies and energy needs.

🧠 Independent Expert Advisory Panel

Renée proposes the creation of an independent advisory panel made up of representatives from:

Industry

Academia

Technical energy experts

Finance

Community

Policy sectors

This panel would guide and review the national energy strategy, ensuring diverse perspectives and consensus-driven decisions.

💡 ETS Reform

The current Emissions Trading Scheme (ETS) is under scrutiny. Renée’s paper calls for:

Removing electricity generation from the ETS to reduce household power bills.

Allowing businesses to reinvest ETS costs into their own decarbonisation efforts.

Applying ETS only when viable alternatives exist.

🥕 Incentives Over Penalties

Rather than punitive measures, Renée advocates for targeted funding and incentives—similar to Australia’s approach. Supporting industry and households in their transition is key to achieving meaningful decarbonisation.

🗳️ Support the Petitions

Renée has launched two petitions to drive change:

📌 Energy Strategy Petition

Calls for a realistic, long-term energy plan that includes both traditional fuels and renewables, with regional flexibility and innovation.

📌 ETS Reform Petition

Challenges the current ETS framework, proposing reforms that reduce costs and empower businesses to invest in sustainable practices.

Renée Jens is urging New Zealanders to support these initiatives and help shape a smarter, more resilient energy future.

All businesses need electricity. All people in a modern society like ours need electricity. The trouble lies in finding balance between combatting climate change and generating enough electricity to sustain our population.

We all know and understand the importance of decarbonizing given the ominous challenge posed to us by climate change globally. But, New Zealand is a small, remote country which only accounts for 1/15th of 1% of the world’s population of 7.5 billion.

New Zealand’s electricity and natural gas markets are inextricably inter-linked. Electricity and gas compete as alternative energy sources, but rely on each other for production. Electricity generation is the second biggest user of natural gas after methanol production by Methanex. Gas is the second biggest source of electricity generation after hydroelectricity.

With this intricate dependence on one another, the effective management of our national energy strategy (including electricity and gas etc) is critically important to our continuing economic health and hence to the well-being of all 5 million kiwis.

What impact does prohibiting natural gas exploration have on New Zealand’s energy supply?

The outright prohibition three years ago of all new offshore oil and gas exploration, is having a profoundly negative impact on the natural gas sector and hence on the health of the electricity sector.

No matter how well intentioned this original decision was, it was not thought through properly at the time. The recent apparent softening of the Government’s stance on the role of natural gas as a transition energy source on the road to 100% renewability is, however, to be commended.

Coal-based electricity generation in 2020 was the highest for a decade.

It’s unfortunate that, as a result of these policies, coal-based electricity generation in 2020 was the highest for a decade. This coincided with the lowest gas-based electricity generation for nine years.

Given that coal emits +/- 1.9 times more CO2, on a gigajoule-for-gigajoule basis than natural gas, this is an environmental step backwards. In this regard, coal imports of +/- 1 million tonnes from Indonesia in 2020 are currently on course to triple in 2021 as we understand it.

What other factors impact New Zealand’s energy mix?

The negative impacts of the above prohibition have unfortunately been compounded by various other negative electricity supply and demand factors since then.

These factors have included:

Rebounding electricity demand following the Global Financial Crisis in 2008.

Back-to-back very dry summers in 2019/20 and 2020/21.

The retirement of thermal powers stations like Otahuhu B and Southdown.

The inability of new renewable power stations to meet the combined challenge posed by growing electricity demand and reduced thermal generation.

Gas and geothermal energy supply in New Zealand is struggling

Pohokura has been our biggest natural gas field for some years. During the past two years however, production has fallen sharply for unspecified technical reasons. This decline in gas production has reduced gas supplies available both for gas users and for electricity generation.

The prohibition of all new offshore oil and gas exploration, has also meant that there will be no offshore oil rigs available in NZ waters until 2022, at the earliest, to identify let alone resolve the ongoing production problems at Pohokura.

Other gas supply options have been constrained in the longer term by the non-renewal by the Government of existing offshore field permits for undeveloped fields, once their initial term had expired. Previously, successive Government’s lead by both major parties renewed these permits unless there was a compelling specific reason not to.

Power companies are passing costs on to businesses

Seriously damaged gas industry morale has also resulted in a combination of reduced/delayed/cancelled capex in existing gas fields.

Competition has essentially collapsed at the big end of the gas market.

The profound uncertainty surrounding the shorter term, let alone longer term, future of the natural gas industry has already resulted in Contact Energy vacating the time of use (TOU) part of the gas market as TOU agreements covering supply to larger customers expire. Two other gas retailers have also declined to quote for supply to various existing TOU customers.

We are also well aware of other very large TOU gas users (not our clients) who have to use natural gas and have been forced onto punitive spot market-related gas pricing. Major electricity-users like Whakatane Board Mills have also had a huge question-mark over their future due to huge gas-related electricity price hikes.

There is still some limited competition in the non-TOU part of the market (impacting smaller customers), albeit at much higher prices. To all intents and purposes, competition has essentially collapsed at the big end of the gas market.

What would Total Utilities recommend?

Looking to the future, New Zealand must formulate an integrated supply/demand energy strategy covering the transition period until 100% renewable energy is achieved in practice. Much like the cross-party Superannuation Accord in the 1990’s, we need a similar cross-party accord now in this vitally important area.

As such, the Government should:

Reverse its previous ill-advised decision not to extend existing gas field permits on undeveloped fields.

Greatly extend the scope of the existing EECA GIDI Fund/ETA initiatives.

Extend the separate Genesis Energy decarbonisation funding initiative to include Mercury and Meridian too.

To conclude, the appetite for future investment in the gas infrastructure is key to improving certainty in the market. Not only does it send signals to the sellers of natural gas but also to major users who are often multinational organisations. If it becomes more apparent that investment will be very limited, these organisations could very well leave NZ prematurely, obviously impacting employment, business activity and tax revenue.

Business and media enquiries can be made to Total Utilities.