Throughout history technological advancement and change that has lasting impacts on humanity has largely come about through critical mass. As a child, I distinctly remember visiting a friends house and seeing their newly installed solar PV system on the roof. 25 years ago, this seemed like the future as I had only seen photos of such things in books about NASA and science fiction.

While some technologies are adopted quickly into day to day life, it seems to be taking an age for solar systems to become common place. Obviously cost is major driver of this but then so too is how seamlessly technology can be integrated into how we live.

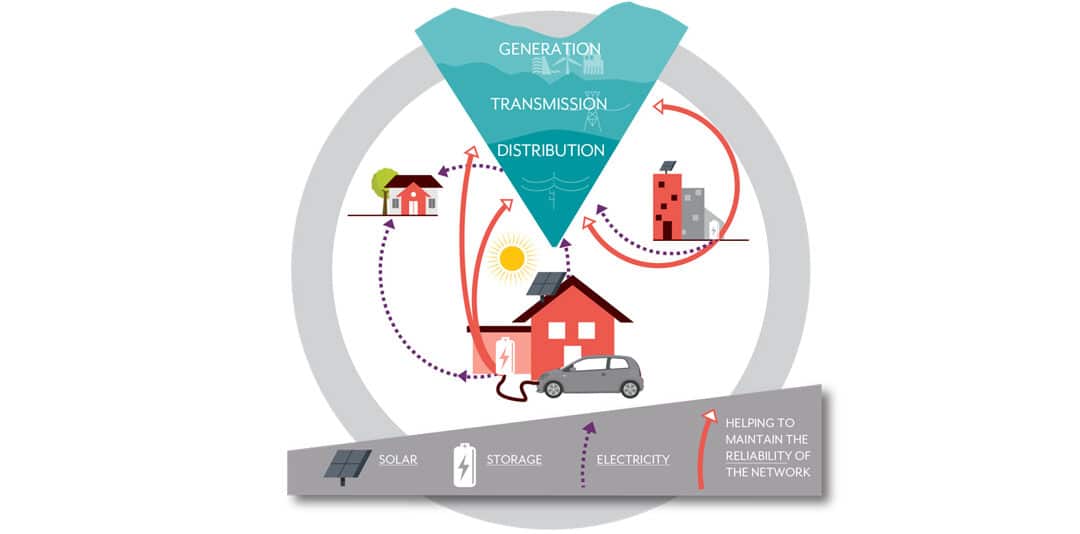

Micro grids have been spoken about in energy circles for some time, but it is only now that the step change in the supply and purchase of energy appears to be gathering momentum as more and more end users are installing solar systems and battery storage.

Contact, Trustpower and Vector have all been trialing various strategies relating to this in Wellington, Tauranga and Waiheke Island respectively. Some third party companies are taking a slightly less traditional approach allowing end users to buy and sell energy directly between each other underpinned by blockchain technology removing the need for a “middle-man” so to speak.

The following post from Centrica has direct parallels with the New Zealand energy market.

Suzanne Schutte is a supermarket worker – and an energy pioneer.

The mother of two from Wadebridge, Cornwall is the first householder to have solar panels and cutting-edge battery technology installed as part of a £19 million trial that aims to help unlock further renewable energy use across her part of south west England.

What makes this scheme different to thousands of other rooftop solar schemes across the world – and what makes Suzanne a pioneer – is that the electricity generated by the solar panels and stored in her battery won’t just be used by her home or sold back into the grid.

Under the Cornwall Local Energy Market, homes and businesses will eventually be able to trade electricity with each other directly. This gives them greater control over their energy use and greater access to cleaner and cheaper electricity.

By taking part in the scheme, Suzanne joins a select band of people in communities across the globe trialling new ways of using and trading energy that are underpinned by the latest digital technology.

Rerouting Renewables

The need for schemes like the Cornwall Local Energy Market has been created by the rise of renewable energy and the inability of existing power grids to move this energy around efficiently.

In most western countries, power transmission networks were developed nearly a century ago to transfer electricity from large coal-fired plants over long distances across the country. However, the map of electricity generation in these countries has changed dramatically over the past decade. For example, renewable energy sources, dominated by wind power, now account for nearly a third of all the electricity generated in the UK.

And microgeneration – where energy is generated by homes or businesses and distributed locally – accounts for 17% of electricity generation.

Government incentives and the falling cost of technology has encouraged many to generate their own power with more than a million homes in the UK using solar panels for their electric and heating needs.

Old-style grids – such as that found in the UK – are not designed to move electricity from thousands of small power plants over short distances. Instead, electricity continues to be fed over long distances to central points in the grid, then fed out again.

This can create curious anomalies. Around the country, many wind farms have had to reduce their power output because of an excess of energy on the grid – due to strong winds and low demand – while major energy consumers including nearby factories have no way of accessing that extra electricity.

Being able to store and move electricity at a far more local level can help smooth out supply and demand, and address many of the problems caused by the intermittent nature of renewable electricity generation.

Going Local

The UK’s National Grid predicts that by 2050 up to 65% of the country’s electricity generation capacity could come from local sources. That means that something needs to change in the way electricity is moved between those producing it and those consuming it.

And this is where schemes like the Cornwall Local Energy Market come in.

The scheme is being funded by Centrica and the European Regional Development Fund, with support from partners including the local distribution network operator and academia. All of the organisations involved regard it as a critical test case for how energy markets around the world could operate in the future.

“The Cornwall Local Energy Market is an important test of how we can better integrate renewable technologies into local areas,” says Ed Reid, Head of Strategy for Centrica Business Solutions.

Reid adds that the opportunity today isn’t only to make the energy system more efficient, but also to give both producers and consumers greater involvement and control.

“The existing energy system is based on 1950s technology and treats the consumer as a passive recipient,” he says.

“It’s far less dynamic than other markets, and I think going forward what we’re seeing with new technologies is that it is allowing customers to be more involved in energy and take better control.”

The Airbnb of Energy

When energy industry experts like Reid talk about making energy more dynamic the way it is in “other markets”, they are referring to the kind of transformation that is currently taking place in sectors such as finance, travel and hospitality.

Specifically, it is the ability for digital technology platforms to enable so-called “peer-to-peer” transactions. In finance it can be seen when, for example, those seeking foreign currency for their holidays can trade their own currency via an app with other travellers.

Arguably the most famous example comes from the hospitality sector, where Airbnb has enabled millions of homeowners to make extra income from renting out their spare rooms.

“Companies like Uber, Airbnb, have really changed the way that we think about business,” says Lawrence Orsini, Founder and CEO of energy blockchain pioneer, LO3 Energy.

“The very same things are happening now at very early stages in energy. We’re seeing more generation on rooftops in our communities, in businesses and that’s going to change the way that business works in the energy industry. It’s really distributing a lot of the power and control to members of communities, and putting more control in the hands of consumers at the edge of the grid.”

Orsini’s company will supply the blockchain technology through which participants in the Cornwall Local Energy Market will be able to trade with each other directly.

LO3’s blockchain for energy empowers consumers to set preferences for energy consumption including local energy produced by neighbours, commercial businesses and farms.

In Brooklyn, residents of the Park Slope and Gowanus neighbourhoods are connected with each other via a virtual microgrid using rooftop solar panels. LO3 has found that consumers want a choice in their energy and believe in creating a stronger, more resilient community focused on local values.

Trading with Blockchain

A blockchain is a database that is shared across a network of computers. It acts as a record of transactions. And because records of those transactions are stored on multiple computers and updated simultaneously, it’s much more secure and harder to hack than a centralised system.

Each transaction is a block, and when the transaction is complete the block gets added to a chain of previous transactions, providing a clear public history of those transactions.

In local energy markets and microgrids, tokens equal to the market value of electricity are traded and logged as transactions or “blocks”. This use of digital tokens means the trade between energy user and producer can happen instantly, without the need for bank approval of the transaction.

For Orsini, this kind of digital communication of data is the key to how grids will function in the future.

A lack of data is one of the main barriers that is stopping people from trading on microgrids, he explains.

“Our devices need to be able to speak to each other about what’s happening on the grid, in order for them to make choices about when they charge, when they discharge, when they produce electricity, how they move electricity. In order to manage the grid of the future, we have to have a significant amount of data. In fact, the grid of the future doesn’t run on coal or natural gas, or wind or solar; it runs on data.”

The Power Plant Next Door

The data vital for energy users and producers to trade locally won’t just come from the supply side. Local energy markets will also be able to understand electricity demand at a far more accurate level than ever before.

UK energy start-up Verv has developed an AI-powered smart hub that sits in people’s homes and learns how much electricity is used by individual devices in the home.

In a trial on a housing estate in Hackney, east London, Verv installed its smart hubs in 40 flats. The information from these boxes is being combined with a blockchain-enabled microgrid that trades the electricity generated by the housing estate’s rooftop solar panels and stored in a communal battery system.

This trial delivered the UK’s first peer-to-peer energy trade using blockchain in April 2018. Verv chief operating officer Maria McKavanagh says having highly detailed knowledge of electricity demand will enable local energy markets to behave like the current wholesale energy market. And that will increase the accuracy of future energy deals.

“We know which appliances are on in real time, how much they’re costing, what’s been used in the past and, therefore, we can predict your future energy requirements much better than we would be able to with smart meters alone,” she says.

That allows customers to buy the amount of energy needed based on a really accurate forecast. Similarly, for the person selling their solar energy, they will be able to ensure they’ve stored enough energy for that day’s needs, and only sell on the excess.

Whether you produce energy or not, schemes like those in Hackney, Brooklyn and Cornwall show how one day we could all become the power plant next door.

The following post was written by Bryan Leyland for KiwiBlog. Bryan is an engineer with over 60 years experience in the energy sector and regularly comments on various topics. He is a strong believer in a single payer market and Carl Hanson, former head of the Electricity Authority argues against this here.

At Total Utilities, we track the competitiveness of contestable costs and been doing so for nearly 20 years. While this data is representative of our customer base (which is made up of small and large commercial and industrial customers and does not include residential customers) we have not seen large “energy” price rises over time. In fact, over-the-counter retail pricing has been relatively flat since the end of 2012 and akin to pricing in 2006. Much of this has been due to increased retail competition in the market providing customers with more alternatives than the traditional “big 4” generator/retailers.

Non-contestable costs, primarily those that relate to the transmission and distribution of energy around the national grid and local grid infrastructure on the other hand, have continued to rise. These monopoly-based costs vary considerably around the country, for example, a typical split nationally between contestable energy and non-contestable pass-through charges is around 60/40. In Top Energy in the far north, it can be the reverse of this. Conversely, Auckland and Wellington the cost split can be 70/30 and in Christchurch 50/50. Regional networks, in the North Island particularly, due to its geographic shape and population imbalance suffer from covering large areas with lower customer density compared to main centers. As such maintaining the network over what can be very rugged and mountainous terrain is expensive.

So where does this leave us, the fundamental issues of the system still remain.

In a normal year, we have enough generation to meet current demand, however dry year future proofing remains an issue given current Government policy.

Natural Gas which is seen overseas as an answer to coal-fired electricity generation will continue to increase in price in NZ as we exhaust current drilling permits and fields come offline.

The Government is looking to try to accelerate the uptake of Electric Vehicles but not talking about the cost of the required upgrades to network infrastructure to support rapid charging. As most rapid charging will be done outside of main centers, this will put increased pressure on more remote areas of the Government-owned Transpower network and local network operators.

The cost of building and consenting new large-scale generation infrastructure well exceeds current wholesale prices that generators can charge. Gas-fired thermal generation or Geothermal generation is far easier to build than a new hydro scheme or wind farm due to the size of its footprint and lower impact on the visual landscape.

Distributed generation such as Solar remains unsuitable for many parts of the country due to a lack of sunshine hours. Businesses would only realise a payback on outlaid capital after 15-20 years in most areas. Batteries are still carbon intensive to manufacture and costly to buy.

There is no magic bullet to ensure long-term security of supply at competitive pricing

The Electricity Price Review has revealed that residential electricity prices have increased by about 80% above inflation since 1990. Why did this happen? We were promised that privatisation and the electricity market would reduce power prices.

An objective examination of the whole electricity industry and the effect of the reforms leads to some interesting conclusions.

Cross subsidies

Before the reforms many power boards cross subsidised residential consumers by overcharging commercial and industrial consumers. The removal of these subsidies is a factor in the increased residential prices.

The market

The Wholesale Market Electricity Development Group made a mistake when they rejected the recommended market model and chose a market that pays all generators the price bid by the most expensive generator selected to run. This would have been a good choice if New Zealand relied entirely on fossil fuel generation. New fossil fuel power stations produce cheaper power than older ones so such a market encourages the construction of new and better stations.

In New Zealand, the cheapest generation comes from old, low cost, depreciated hydro stations. The choice of a fossil fuel market structure pays these stations the much higher price needed by the most expensive fossil fuel station. Hydro stations then rack up their asset values to camouflage the fact that they are making windfall profits

The recommended market model would have ensured that consumers would have continued to get low-cost electricity from the hydro stations that they had already paid for and built new stations that would give the lowest system costs in the long run.

The chosen market structure has led to wholesale prices increasing when they should have decreased to reflect the major reductions in operation and maintenance cost that followed on from privatisation.

Control of peak demand

Before the electricity reforms all electric water heaters in New Zealand were remotely controlled by the lines companies to reduce system peak demand by more than 10%. The reforms destroyed this world leading system. Most lines companies abandoned water heater control because the reforms did not allow them to fully recover of the costs of operating, maintaining and expanding the hot water control system.

As a result of abandoning hot water control, new power stations and a $960 million 400 kV line into Auckland were needed and millions more were spent on reinforcing transmission lines and distribution systems. All this to meet a peak demand that would not have existed with the recommended market.

Assets revalued

The reforms also allowed Transpower and lines companies to massively revalue their assets and use this increased value to justify charging consumers millions of dollars more for assets that consumers had largely paid for already. This is a major factor in the increased cost of electricity.

Traders and retailers

The electricity market also brought us traders and retailers who, it can be argued, serve no useful purpose whatsoever. The recommended market model did not need them.

In our market, traders often compete to get selected to generate. But when generation is in short supply competition is virtually non-existent and the price that they bid is “a trade-off between greed and guilt”. (On several occasions in the last few weeks wholesale prices have spiked to more than 10 times the normal price for no apparent reason.) As two retiring CEOs pointed out, the way to make money in the New Zealand market is to keep the system on the edge of a shortage. With the recommended market the system operator would have ensured that sufficient generating capacity was available and selected the generators that would give a reliable supply at the lowest cost.

Retailers increase consumer costs by spending millions of dollars trying to steal consumers from each other and pretending to compete in selling a commodity that is identical for everyone.

Conclusion

So what of the future? It does not look good. Transpower has warned that the risk of serious shortages and high prices in a dry year is rapidly increasing and no one has plans for new power stations that would mitigate this risk.

The government ignores dry year risk because it is hellbent on shutting Huntly down and limiting gas supplies and believes that exploiting wind and solar power will solve all the problems. Never mind that they are much more expensive, require backup when the wind doesn’t blow or the sun doesn’t shine and don’t make any useful contribution to meeting peak demand.

The best and cheapest way of mitigating the risk of blackouts in dry years is to ensure that Huntly continues to provide dry year reserve with two or three generating sets and 1 million tons of coal available.

The government should be taking steps to make sure that we have an economical and reliable supply into the future. If it wants to reduce CO2 – a gas that promotes plant growth and benefits our agricultural industries – it should contemplate the construction of a major and very expensive hydro pumped storage power station in the hills above Roxburgh that would solve the dry year problem. Only then can it ditch Huntly.

The New Zealand electricity market is a classic example of what happens when the politicians and the decision-makers do not understand power systems and how difficult it is to provide a reliable and economic supply. Choosing the wrong market model has cost the customer dearly.

In this exclusive series of articles by David Spratt, he explores the electric vehicle (EV) options for specific business uses.

Part 3: Evaluating the Volkswagen e-Golf electric car.

It may be that I have now test driven one too many electric vehicles (EVs), but I have become increasingly irritated by the clunky and, dare I say, ugly designs that have been rolled out by some manufacturers.

Not the e-Golf, though. Volkswagen addresses this design challenge with a vehicle that feels familiar, comfortable and accessible from the moment you climb into it. Built from the ground up to look, feel and handle like a standard Golf Super Mini, this smart town car is a delight.

I want a car that can take me safely along country roads while allowing me to travel to the city, park in tight parking spots and save money on fuel. The e-Golf ticks every one of these boxes.

It accelerates smoothly and relatively quickly (from 0 to 100kph in 9.6 seconds).

It also has, for a small car, decent boot space and plenty of leg room for front and back seat passengers. I am six feet tall (1.83 metres for those of you living in the 21st century) and found the front and rear seating gave me plenty of leg room and riding comfort. My wife, a not-so-tall person, had an issue with seeing over the steering wheel for a clear view of the road ahead. But a simple height adjustment for the seat would have addressed this issue.

I live in the rural outskirts of Auckland and so want a car that can take me safely along country roads while allowing me to travel to the city, park in tight parking spots and save money on fuel. The Volkswagen e-Golf ticks every one of these boxes.

If I was to be critical though, there were occasions when the car’s electronics got themselves into a bit of a twist and just stopped working. On at least two occasions, the parking brake and the auto hold feature for hill starts went to war, leaving me stuck in one place with a warning light and screeching sound, raising my anxiety levels. In the end, the only answer seemed to be to switch everything off and start again: fine if you are in a parking lot but not great if you are pulling out into traffic. This may be the result of an idiot behind the wheel rather than a fault, but it happened to both me and my wife on separate occasions.

Are we there yet?

Range anxiety was also an issue with the e-Golf’s distance calculator.

One moment my predicted range was displayed as 157km, then a few minutes later was 140km, only to return to 150km a while after that. I put this down to the range calculator being very sensitive to driving style and conditions, but a bit less variability would have had me more focussed on the road and less on worry about getting home on the available charge.

But charging was a breeze. At home, using a simple three-pin connector, a total recharge took around 11 hours. My favourite, free, fast charger at Counties Power HQ took 45 minutes to get me up to 80 percent, plenty of time for a coffee and a quick browse around the shops nearby.

As is the case with all the electric vehicles I have tested, the e-Golf saw me spending less than $20 per week on charging with no concessions to convenience.

Despite the car’s price of $65,990 the economics for the average business owner almost make sense. Give it a year or two and EVs like this will be a no-brainer for many business applications.

My contacts tell me the Volkswagen e-Golf is rapidly becoming a European sensation, and the future of VW motoring. I can see why. This car is a little beauty.

I gave the Volkswagen e-Golf an admiring 7.5 out of 10.

Thanks to VW New Zealand for supplying the e-Golf for testing.

In this exclusive series of articles by David Spratt, he explores the electric vehicle (EV) options for specific business uses.

Part 2: Evaluating the Tesla Model S P100D electric car

What do you get when you mix an eccentric, Los Angeles-based, internet billionaire with the desire to build an electric vehicle with speed and acceleration to challenge the world’s top performance cars?

The answer is the Tesla 100S, complete with vegan leather seats and “bio-weapon defence mode” to keep the car’s air fresh in case of anthrax attack.

I started test-driving the Tesla S (P100D model) with a mixture of excitement and trepidation. Excitement because I knew this vehicle could take me from zero to 100kph in less than three seconds; and trepidation because of the $250,000 price tag and more personally the $5,000 insurance excess I agreed to when I signed for the car test.

After a week, the fear of crashing a car worth more than the deposit on a Ponsonby house had almost completely gone but the sheer thrill of an EV accelerating in Tesla’s infamous, “Ludicrous” mode remained days after I tearfully gave the car back.

Long range

So, what makes the P100D so special apart from its raw power? First is the range. This beast will travel from Auckland to Taupo and back on a single charge. That’s 600km.

Despite reservations about charging and spare tyres, the Tesla 100S is, bar none, the most exciting and innovative car I have ever driven.

There is a downside though. Recharging the 100kW battery from empty in your garage power point means a 36-hour wait. But for around $8,000 you can install a special Tesla charger at home that dramatically reduces this time.

After failing the home charging test, I resorted to Tesla’s free charging stations (there are six across the country, with many more to come). This will recharge from empty in less than an hour.

I also tried using the Counties Power free charger in Pukekohe, only to discover that the Tesla charging cable requires a special adapter to fit standard charging stations. As this adaptor was not provided, I skulked home and resorted to an overnight top-up before driving to town and the Tesla service centre, where the unfailingly helpful people charged my car and provided the adaptor.

No dirty hands

Speaking of not provided. The Tesla Model S has no spare tyre. Instead you push the help button, and someone turns up and changes it for you! This service comes free for the life of the car and includes towing you home if you run out of electric charge. Ah to be that rich!

When driving I felt safe and in control throughout, even around the challenging corners of Auckland’s Waitakere Ranges. Traction control, adjustable suspension and the stabilising weight of the Mosel S’s powerful batteries made for responsive handling and comfortable road feel, this despite the Tesla’s extraordinary performance characteristics.

The Tesla even comes with “Santa mode”: listen to Christmas carols and glimpse a sleigh pulled by reindeer on the screen while winding the car out to a top speed of over 250kph (in controlled conditions at Hampton Downs racetrack of course).

The bottom line. Despite reservations about charging and spare tyres, the Tesla S is, bar none, the most exciting and innovative car I have ever driven. With companies like Tesla driving change, the future of the EV is in safe hands.

I give the Tesla Model S an ecstatic 8.5/10.

*Thanks to Tesla NZ for providing the Tesla S model for trial. For all the specifications visit www.tesla.com

During the recent two-day EMANZ Conference that I attended in Auckland with our Energy Manager, Tânia Coelho, I was struck by the surge of genuine enthusiasm for and commitment to renewable energy from the diverse group of Energy Managers and others who attended.

In this regard, our country is in the fortunate position that 85% of our electricity supply already comes from renewable energy, mainly hydro-electricity, geothermal and wind-generation based.

Successive National and Labour Coalition Governments have made a strong and binding commitment to New Zealand meeting its global carbon emission reduction obligations.

To achieve these commitments in practice, New Zealand will need a sustained and integrated programme, to utilise rapidly evolving technology in this area.

The following guest post by James Flexman, Wholesale Markets Manager, Mercury highlights some of the excellent work in the inter-related areas of solar power and battery storage, that their company is championing.

Innovative Battery Technology Has Potential to Disrupt Fundamental Aspect of Electricity Market

The crazy thing about the electricity market, the thing that sets it apart from almost all other markets, is its immediacy. Electrons are the ultimate NOW product. They’re right here, right now, turn on the switch, see the light.

New Zealand’s sophisticated spot market and all its intricacies have been developed to work with electricity’s time-bound quirk of physics and deliver reliable, affordable and mostly renewable electricity to Kiwi homes and businesses.

But now this non-negotiable is being challenged. There’s a ‘disruptive technology’ on the scene that, like a kind of Timelord, has the potential to substantially diminish the impact of time and timing on the generation, dispatch and ultimate use of electricity. We’re talking about the exciting new opportunity created by super-batteries that can charge up with electricity from the grid and store it, before being re-dispatched into the electricity market.

Grid-Connected Battery Research & Development

Last week Mercury launched its own 1MW/2MWh battery storage facility at our R&D centre in South Auckland. For context 2MWh of electricity could power 400 homes for a winter evening peak for 2 hours. On its own, it’s not going to change the world and it’s also definitely not for the short-term gain. The rate of return based on trading 2MWh of electricity in and out of the national grid means it would take many years to break even on the $3 million investment.

Being directly connected to the grid, and able to send energy into the market like a little 1MW power station makes this battery a Kiwi first. And there’s potential for much more.

So what are we expecting in the medium to long-term from this pilot?

The clue is in where the battery has been installed – in Mercury’s R&D Centre in South Auckland. For us, it’s all about the ‘R’ part of ‘R&D centre’: Research. And at a time when the Government is calling for greater investment in R&D in this country, I’d like to do a quick shout-out celebrating the constant ongoing investment in R&D undertaken by Kiwi businesses every day of the week.

The battery is a pilot, a toe in the water, part of the New Zealand electricity market’s ongoing exploration of battery storage as the technology evolves, to work out what part batteries will play in the energy generation eco-system of this country. We believe there’s potential here. Reflecting on the first generation in New Zealand (for power, not gold processing) at Reefton, it was a 20kW generator – and look what hydro generation has grown to and its role in our economy now.

Battery Pilot a Milestone for Innovation

And it’s a true innovation. Mercury is the first company in New Zealand to install a battery system that is directly connected to Transpower’s high voltage national grid and to use the battery to participate in both the energy and reserves markets. Others have explored other ways that battery storage could interact with our current energy landscape – Counties Power together with Genesis, Vector and Alpine Energy have all commissioned batteries that can participate in the energy market, but these are also used to manage local networks better.

Being directly connected to the grid, and able to send energy into the market like a little 1MW power station makes this battery a Kiwi first. And there’s potential for much more. The storage facility is on the site of Mercury’s mothballed thermal power station next door to Transpower’s Southdown switchyard which is capable of moving over 100MW in and out of the grid.

However, despite the facility being able to accommodate battery storage of this size (similar to the much publicised South Australian battery project that Tesla committed to (and did) build within 100 days), trading at this scale will only start once the R (Research) has turned to D (Development). But once this happens, (when battery technologies develop further and costs of large-scale batteries drop), the lessons we have learnt from our investment in 2018 will give us a fast start to capitalise on this exciting opportunity.

Grid-Connected Battery Research May Lead to Paradigm Shift

There is also some other work that Mercury has been doing that will benefit us as well as all future battery traders. This work (which also involves Transpower and the Electricity Authority) is addressing current regulations that need to be adjusted to accommodate the participation of battery stored electricity in all aspects of the NZ reserves market.

The use of large-scale batteries to store energy from times of lower usage and make it available when it’s most needed could make a real difference to the way power is supplied to homes and businesses over the coming decades, particularly as populations grow. At scale, the lowest parts of the demand curve will be raised as electricity will be generated and stored in batteries and the highest peaks of demand will be offset by electricity being re-dispatched from the batteries back into the market.

In a future world, when the investment that companies like Mercury are making in R&D has led to large-scale battery storage in New Zealand, this flattening of the supply-demand curve should lead to more efficient use of current generation capacity.

We see all these future developments as great reasons for our research investment now. And we’re proud to be pioneers in this field that has so much potential to change the New Zealand energy market to everyone’s benefit.

See how the direct grid-connected battery will work in New Zealand’s energy eco-system

In this exclusive new series of articles, I explore the electric vehicle (EV) options for specific business uses. We are grateful to the car companies* for supplying their EVs to test-drive, charge and parade around Auckland.

Part 1: Evaluating the BMW i3 electric vehicle

The reality for all businesses is that electric vehicles (EVs) have to deliver on the promise of performance, economics and relevance. Many business vehicles never leave town. Whether they are driven from business to business by busy salespeople or thrashed by couriers, what is required is a car that is reliable, fuel-efficient and a bit good looking.

That’s a tough call, up against an existing petrol range of cool kids like the Suzuki Swift, Honda Jazz and VW Polo: especially when new, entry-level petrol models sell for around $20,000 and the i3 costs about $75,000.

Price is not the only factor though.

To test the distance range capability of the i3 I arranged meetings involving a 120km return trip across town: Drury to Albany at peak hour. With the car’s stated range of 180km, I have to say that on my first trip I was not filled with confidence. I wondered whether the i3 could take on the challenge of sitting in that giant carpark known as Auckland’s motorway system, without my ending up on the side of the road, with a flat battery and subjected to the shaking fists of irate rubberneckers.

At the end of that day, I had travelled 120km at the speed of a lame greyhound in nose-to-tail traffic yet ended up with a remaining range of 127km. So, to travel 120km I used 53km of range. This sounds impossible, but the i3 cleverly uses the stop-start acceleration and braking to recharge its batteries – and there was lots of that going on.

Lookin’ good: what’s great about the BMW i3 electric vehicle

The two-door BMW i3 looks sleek, Euro and sophisticated. The software features are very cool, guiding you to the nearest charging station and, if required, planning your route to ensure you don’t end up using the optional two-cylinder petrol backup engine to limp home. The auto-park feature is also excellent, if a little scary the first time you take your hands off the wheel and trust the computer.

Charging it in my garage overnight was a breeze – just plug it into a three-pin socket and walk away. Just as easy was the 30-minute rapid charge at Counties Power in Pukekohe. I literally plugged it in, walked across the road, ordered and drank a cup of tea and returned to a vehicle recharged for free!

I mention free fast chargers and easy home charging for context. The i3 is energy efficient, saving masses of money on fuel, especially since the new local fuel tax had just kicked in. On average each week I spend around $150 on petrol. In the week I had the i3 my electricity bill went up by $10 while my Commodore sat sulking at home consuming no petrol. On an annual basis that’s a fuel saving of $7280. With residual value and fuel savings the economics of an EV look pretty good.

Money savings on petrol stack up quickly.

Uh oh: problems with the BMW i3 electric vehicle

On the downside, the i3 handles like it is skidding on marbles. Maybe it’s the unusually large wheels, designed to generate more energy, but I never felt comfortable behind the steering wheel in this regard. Road-holding was fine at lower speeds around town but very disconcerting on the open road.

For such an externally large vehicle there is not a heap of room for back seat passengers or for luggage in the boot. Space wise it felt like a reverse TARDIS – bigger on the outside than on the inside.

Overall the i3 appears as if HQ in Germany identified the need to make an electric vehicle but gave the job to a bunch of petrol heads who hadn’t signed up for building a hippy, nippy town car.

BMW: for $75,000 you can do a lot better. Having said that, the first internal combustion cars weren’t exactly things of beauty either.

I gave it a solid 6/10.

*The BMW i3 was kindly provided by BMW and Contact Energy. For detailed specifications visit bmw.co.nz.

Suzanne Schutte is a supermarket worker – and an energy pioneer.

The need for schemes like the Cornwall Local Energy Market has been created by the rise of renewable energy and the inability of existing power grids to move this energy around efficiently.

The UK’s National Grid predicts that by 2050 up to 65% of the country’s electricity generation capacity could come from local sources. That means that something needs to change in the way electricity is moved between those producing it and those consuming it.

When energy industry experts like Reid talk about making energy more dynamic the way it is in “other markets”, they are referring to the kind of transformation that is currently taking place in sectors such as finance, travel and hospitality.

A blockchain is a database that is shared across a network of computers. It acts as a record of transactions. And because records of those transactions are stored on multiple computers and updated simultaneously, it’s much more secure and harder to hack than a centralised system.

The data vital for energy users and producers to trade locally won’t just come from the supply side. Local energy markets will also be able to understand electricity demand at a far more accurate level than ever before.