This figure also applied to the tens of thousands of small businesses using small amounts of electricity. What followed was a studied silence from the industry.

There has subsequently been a great deal of debate and finger-pointing as to just who is responsible for an electricity market that delivers average monthly bills of around $300 to Kiwi households, while our Melbourne, Australia, cousins are charged roughly the same price per quarter!

All this while Aussie generators are burning expensive and polluting coal, gas and oil to meet demand, and we mainly use sustainable hydro generation that has paid for itself many times over.

Business Impacts

As business people, we are not immune from this unresponsive market. Our staff are consumers too and their budget pressures impact wage demands. We are also just the last cab off the rank when it comes to increased electricity price charges.

If you signed a new, fixed price, 24-month electricity contract last September you will now be paying around 20 per cent less for electricity than if you signed a similar contract today. Everything indicates that this trend in the commercial market will continue as the industry continues to “adjust” prices skywards.

The Power Players

There are several players that influence our electricity market. Let’s start with the retailers. Most of us are aware of so-called “prompt payment discounts” that offer between 10 and 20 per cent lower pricing if we pay on time. For individuals or businesses under financial pressure these discounts can often be unattainable as the need to pay staff, taxes or put food on the table trumps their ability to pay by a given date.

What many of us don’t realise is that these discounts are often not discounts at all. The retailer has just loaded the “discount” onto their usual rate, leaving the late payer under even more cost pressure.

To their credit Meridian announced an end to this practice last September. The price review panel chimed in last month and called for an end to this practice altogether.

To Switch or Not to Switch?

There are also the much advertised switching campaigns that try to persuade consumers and small businesses to switch suppliers in the hope of getting a better deal. This is a complete fallacy for small businesses and households under financial pressure. While retailers are only too happy to accept businesses or individuals with good credit records, they simply decline switch applications from distressed payers.

It could be said that’s the outcome of paying bills late but in many cases credit checks will, at a time when they need to watch every dollar, exclude people or businesses from beneficial pricing.

Many retailers have also, until recently, offered significant incentives to stop customers from switching. Fair enough, you might think, except that businesses that pay their bills on time and loyally stick with their preferred supplier are not offered these incentives, and so end up paying more despite being great customers.

This, along with many other structural impediments, is exactly why Ms Dean QC and her team are finally taking a long, hard look at how our electricity market functions. This year’s energy price review should prove interesting!

[Electricity] Demand has, year on year, been steadily rising. This trend is likely to continue, so don’t look for much relief from higher electricity prices in the near term.

I recently talked to a businessperson who had signed up to an electricity contract that had his company effectively speculating on the spot market.

What the company didn’t realise (and wasn’t told) was that playing the electricity spot market was fraught with upside cost risk. In their case they are now paying more than three times the standard retail electricity rate for business, and facing significant fees if they attempt to get out of the contract.

What disappointed me in this case was that the consultant they paid for advice also took a trailing commission from the electricity service provider. In other words, no-one was representing the client’s best interests in a transaction that was fraught with risk.

Let’s talk about the situation our businessman faces and how it came about that the company is locked into a contract that will potentially cost it tens of thousands of dollars more than a simple retail contract offered.

It comes down to supply, demand and price uncertainty.

How the electricity spot market works

Most of our electricity is provided via South Island lakes. Lake water has remained at average levels for the time of year right through the summer period thus far. What has driven the price escalations is thermal outages. A large chunk of North Island thermal generation plant has been unavailable due to maintenance.

What was scheduled as a short-term outage has turned into longer ones as issues have been found that are taking time to remediate.

Even when it is running at full capacity, thermal generation is more expensive than hydro. The wholesale price of gas is escalating, and the price of coal has effectively doubled since 2016. The impact of this means that generators are less likely to offer thermal generation to the market if prices are low. Hydro has, therefore, been used through the year, reducing the ability for hydro generators to conserve water when the pressure went on summer lake levels.

National demand has also increased significantly. This summer so far, demand is the highest it has been in the past four years. Demand has, year on year, been steadily rising. This trend is likely to continue, so don’t look for much relief from higher electricity prices in the near term.

It’s not entirely bad news though. Even in a time of escalation, fixed prices have remained below where we were at this time in 2012. There was a significant market correction towards the end of that year and businesses have benefitted from attractive electricity pricing since.

Should we enter the spot market?

What does this mean for those businesses whose contracts have expired or will expire soon?

Unless they have an energy expert on staff, they need to think very hard before entering contracts that lock them into variable pricing based on the electricity spot market.

Negotiating an electricity contract can be complex. Good advice can save a business thousands, if not tens or even hundreds of thousands of dollars, depending on the size of the business and its energy use profile. Business should use a reputable advisor but be certain that he/she only represents the business’ interests.

Right now, and for the rest of 2019 at least, I suggest a fixed term, fixed price contract wherever possible. Yes, business may pay a small premium in some cases but there are numerous, reputable electricity retail firms that offer good pricing and carry the upside risk for their clients.

The XLS currently retails at $50,990 plus on-road costs (NZD). This puts it right in the sweet spot for businesses looking for a workhorse, four-wheel drive SUV.

Unlike two years ago when high prices and low residuals were a real turnoff for businesses, electric and hybrid SUVs are now in high demand on the second-hand market, and my industry contracts confirm premium trade in prices and strong lease residuals.

Lease companies’ reservations about financing EVs and PHEVs have largely evaporated.

The XLS combines a 2l petrol engine with twin electric motors, giving you a theoretical fuel efficiency of 1.7 litres of petrol per 100km travelled. In theory if you were running the electric motor only and never exceeded its specified range of 54km, then this incredible efficiency is quite possible.

However, in Auckland motorway traffic, I found a single tank of gas and a $1.50 overnight charge got me well over 700km or 6.43 litres of fuel for every 100km travelled: still an excellent range result by any measure.

Pragmatic manufacturing

When I drained the EV battery the XLS automatically switched to petrol power. It also offered the option of “charge” mode that used the petrol engine, engine braking and inertia, to recharge the electric motor. This proved more expensive in fuel usage but was convenient, simple and practical – Japanese manufacturing at its most pragmatic.

Charging has often been a bone of contention for users hooked on the convenience of petrol stations. This PHEV delivered a fast charge to 80 per cent in just 20 minutes. As fast chargers become more common the convenience gap should be a minor irritant for most users. We will have to alter our behaviours a little though.

Mitsubishi now offers a 160,000km, five-year warranty on the motor and an eight-year warranty on the battery. This largely matches the warranties offered for their petrol and diesel options.

So enough of the technicalities. What did I and the love of my life think of this Japanese invader? For me, words like practical, common sense, hardworking and efficient come to mind. My beloved liked the excellent visibility from both front and rear seats, the sensitive steering and braking and the fact that the vehicle looked stylish without losing its fundamental functionality.

We both loved the spacious leg room and fold-down seats for carrying luggage, samples and tools in the back.

We didn’t like the oddly small driver’s rear vision mirror. The acceleration and sustained performance that we have come to expect from electric vehicles wasn’t to the fore either. Not that the XLS was underpowered, it’s just that when you are used to the romance and zip of a pure electric motor the hybrid felt a bit like kissing your sibling: underwhelming.

Overall, I really liked this solid addition to the SUV fleet.

The years 2019 and 2020 will see big moves from Asian manufacturers into the EV market. Soon the combined price, residuals, fuel efficiency, reliability and convenient charging of hybrid and pure electric vehicle categories will make the business case very compelling for New Zealand enterprises looking to drive out costs, reduce capital deployed and contribute to a sustainable world for future generations.

Businesses will do well to keep a close eye on how they can reap the benefits.

I gave the Mitsubishi XLS PHEV a sturdy 7.5 out of 10.

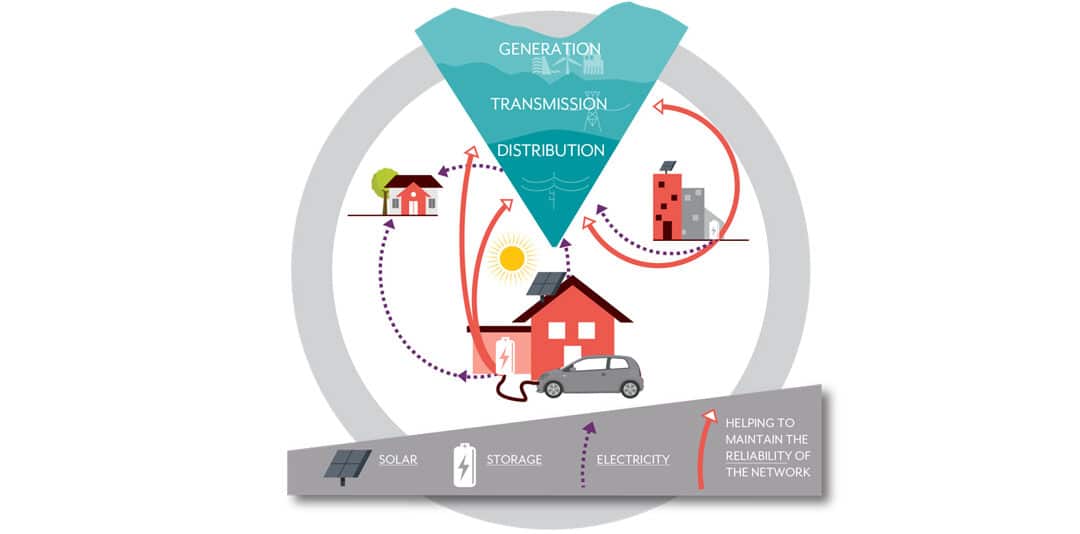

Throughout history technological advancement and change that has lasting impacts on humanity has largely come about through critical mass. As a child, I distinctly remember visiting a friends house and seeing their newly installed solar PV system on the roof. 25 years ago, this seemed like the future as I had only seen photos of such things in books about NASA and science fiction.

While some technologies are adopted quickly into day to day life, it seems to be taking an age for solar systems to become common place. Obviously cost is major driver of this but then so too is how seamlessly technology can be integrated into how we live.

Micro grids have been spoken about in energy circles for some time, but it is only now that the step change in the supply and purchase of energy appears to be gathering momentum as more and more end users are installing solar systems and battery storage.

Contact, Trustpower and Vector have all been trialing various strategies relating to this in Wellington, Tauranga and Waiheke Island respectively. Some third party companies are taking a slightly less traditional approach allowing end users to buy and sell energy directly between each other underpinned by blockchain technology removing the need for a “middle-man” so to speak.

The following post from Centrica has direct parallels with the New Zealand energy market.

Suzanne Schutte is a supermarket worker – and an energy pioneer.

The mother of two from Wadebridge, Cornwall is the first householder to have solar panels and cutting-edge battery technology installed as part of a £19 million trial that aims to help unlock further renewable energy use across her part of south west England.

What makes this scheme different to thousands of other rooftop solar schemes across the world – and what makes Suzanne a pioneer – is that the electricity generated by the solar panels and stored in her battery won’t just be used by her home or sold back into the grid.

Under the Cornwall Local Energy Market, homes and businesses will eventually be able to trade electricity with each other directly. This gives them greater control over their energy use and greater access to cleaner and cheaper electricity.

By taking part in the scheme, Suzanne joins a select band of people in communities across the globe trialling new ways of using and trading energy that are underpinned by the latest digital technology.

Rerouting Renewables

The need for schemes like the Cornwall Local Energy Market has been created by the rise of renewable energy and the inability of existing power grids to move this energy around efficiently.

In most western countries, power transmission networks were developed nearly a century ago to transfer electricity from large coal-fired plants over long distances across the country. However, the map of electricity generation in these countries has changed dramatically over the past decade. For example, renewable energy sources, dominated by wind power, now account for nearly a third of all the electricity generated in the UK.

And microgeneration – where energy is generated by homes or businesses and distributed locally – accounts for 17% of electricity generation.

Government incentives and the falling cost of technology has encouraged many to generate their own power with more than a million homes in the UK using solar panels for their electric and heating needs.

Old-style grids – such as that found in the UK – are not designed to move electricity from thousands of small power plants over short distances. Instead, electricity continues to be fed over long distances to central points in the grid, then fed out again.

This can create curious anomalies. Around the country, many wind farms have had to reduce their power output because of an excess of energy on the grid – due to strong winds and low demand – while major energy consumers including nearby factories have no way of accessing that extra electricity.

Being able to store and move electricity at a far more local level can help smooth out supply and demand, and address many of the problems caused by the intermittent nature of renewable electricity generation.

Going Local

The UK’s National Grid predicts that by 2050 up to 65% of the country’s electricity generation capacity could come from local sources. That means that something needs to change in the way electricity is moved between those producing it and those consuming it.

And this is where schemes like the Cornwall Local Energy Market come in.

The scheme is being funded by Centrica and the European Regional Development Fund, with support from partners including the local distribution network operator and academia. All of the organisations involved regard it as a critical test case for how energy markets around the world could operate in the future.

“The Cornwall Local Energy Market is an important test of how we can better integrate renewable technologies into local areas,” says Ed Reid, Head of Strategy for Centrica Business Solutions.

Reid adds that the opportunity today isn’t only to make the energy system more efficient, but also to give both producers and consumers greater involvement and control.

“The existing energy system is based on 1950s technology and treats the consumer as a passive recipient,” he says.

“It’s far less dynamic than other markets, and I think going forward what we’re seeing with new technologies is that it is allowing customers to be more involved in energy and take better control.”

The Airbnb of Energy

When energy industry experts like Reid talk about making energy more dynamic the way it is in “other markets”, they are referring to the kind of transformation that is currently taking place in sectors such as finance, travel and hospitality.

Specifically, it is the ability for digital technology platforms to enable so-called “peer-to-peer” transactions. In finance it can be seen when, for example, those seeking foreign currency for their holidays can trade their own currency via an app with other travellers.

Arguably the most famous example comes from the hospitality sector, where Airbnb has enabled millions of homeowners to make extra income from renting out their spare rooms.

“Companies like Uber, Airbnb, have really changed the way that we think about business,” says Lawrence Orsini, Founder and CEO of energy blockchain pioneer, LO3 Energy.

“The very same things are happening now at very early stages in energy. We’re seeing more generation on rooftops in our communities, in businesses and that’s going to change the way that business works in the energy industry. It’s really distributing a lot of the power and control to members of communities, and putting more control in the hands of consumers at the edge of the grid.”

Orsini’s company will supply the blockchain technology through which participants in the Cornwall Local Energy Market will be able to trade with each other directly.

LO3’s blockchain for energy empowers consumers to set preferences for energy consumption including local energy produced by neighbours, commercial businesses and farms.

In Brooklyn, residents of the Park Slope and Gowanus neighbourhoods are connected with each other via a virtual microgrid using rooftop solar panels. LO3 has found that consumers want a choice in their energy and believe in creating a stronger, more resilient community focused on local values.

Trading with Blockchain

A blockchain is a database that is shared across a network of computers. It acts as a record of transactions. And because records of those transactions are stored on multiple computers and updated simultaneously, it’s much more secure and harder to hack than a centralised system.

Each transaction is a block, and when the transaction is complete the block gets added to a chain of previous transactions, providing a clear public history of those transactions.

In local energy markets and microgrids, tokens equal to the market value of electricity are traded and logged as transactions or “blocks”. This use of digital tokens means the trade between energy user and producer can happen instantly, without the need for bank approval of the transaction.

For Orsini, this kind of digital communication of data is the key to how grids will function in the future.

A lack of data is one of the main barriers that is stopping people from trading on microgrids, he explains.

“Our devices need to be able to speak to each other about what’s happening on the grid, in order for them to make choices about when they charge, when they discharge, when they produce electricity, how they move electricity. In order to manage the grid of the future, we have to have a significant amount of data. In fact, the grid of the future doesn’t run on coal or natural gas, or wind or solar; it runs on data.”

The Power Plant Next Door

The data vital for energy users and producers to trade locally won’t just come from the supply side. Local energy markets will also be able to understand electricity demand at a far more accurate level than ever before.

UK energy start-up Verv has developed an AI-powered smart hub that sits in people’s homes and learns how much electricity is used by individual devices in the home.

In a trial on a housing estate in Hackney, east London, Verv installed its smart hubs in 40 flats. The information from these boxes is being combined with a blockchain-enabled microgrid that trades the electricity generated by the housing estate’s rooftop solar panels and stored in a communal battery system.

This trial delivered the UK’s first peer-to-peer energy trade using blockchain in April 2018. Verv chief operating officer Maria McKavanagh says having highly detailed knowledge of electricity demand will enable local energy markets to behave like the current wholesale energy market. And that will increase the accuracy of future energy deals.

“We know which appliances are on in real time, how much they’re costing, what’s been used in the past and, therefore, we can predict your future energy requirements much better than we would be able to with smart meters alone,” she says.

That allows customers to buy the amount of energy needed based on a really accurate forecast. Similarly, for the person selling their solar energy, they will be able to ensure they’ve stored enough energy for that day’s needs, and only sell on the excess.

Whether you produce energy or not, schemes like those in Hackney, Brooklyn and Cornwall show how one day we could all become the power plant next door.

The following post was written by Bryan Leyland for KiwiBlog. Bryan is an engineer with over 60 years experience in the energy sector and regularly comments on various topics. He is a strong believer in a single payer market and Carl Hanson, former head of the Electricity Authority argues against this here.

At Total Utilities, we track the competitiveness of contestable costs and been doing so for nearly 20 years. While this data is representative of our customer base (which is made up of small and large commercial and industrial customers and does not include residential customers) we have not seen large “energy” price rises over time. In fact, over-the-counter retail pricing has been relatively flat since the end of 2012 and akin to pricing in 2006. Much of this has been due to increased retail competition in the market providing customers with more alternatives than the traditional “big 4” generator/retailers.

Non-contestable costs, primarily those that relate to the transmission and distribution of energy around the national grid and local grid infrastructure on the other hand, have continued to rise. These monopoly-based costs vary considerably around the country, for example, a typical split nationally between contestable energy and non-contestable pass-through charges is around 60/40. In Top Energy in the far north, it can be the reverse of this. Conversely, Auckland and Wellington the cost split can be 70/30 and in Christchurch 50/50. Regional networks, in the North Island particularly, due to its geographic shape and population imbalance suffer from covering large areas with lower customer density compared to main centers. As such maintaining the network over what can be very rugged and mountainous terrain is expensive.

So where does this leave us, the fundamental issues of the system still remain.

In a normal year, we have enough generation to meet current demand, however dry year future proofing remains an issue given current Government policy.

Natural Gas which is seen overseas as an answer to coal-fired electricity generation will continue to increase in price in NZ as we exhaust current drilling permits and fields come offline.

The Government is looking to try to accelerate the uptake of Electric Vehicles but not talking about the cost of the required upgrades to network infrastructure to support rapid charging. As most rapid charging will be done outside of main centers, this will put increased pressure on more remote areas of the Government-owned Transpower network and local network operators.

The cost of building and consenting new large-scale generation infrastructure well exceeds current wholesale prices that generators can charge. Gas-fired thermal generation or Geothermal generation is far easier to build than a new hydro scheme or wind farm due to the size of its footprint and lower impact on the visual landscape.

Distributed generation such as Solar remains unsuitable for many parts of the country due to a lack of sunshine hours. Businesses would only realise a payback on outlaid capital after 15-20 years in most areas. Batteries are still carbon intensive to manufacture and costly to buy.

There is no magic bullet to ensure long-term security of supply at competitive pricing

The Electricity Price Review has revealed that residential electricity prices have increased by about 80% above inflation since 1990. Why did this happen? We were promised that privatisation and the electricity market would reduce power prices.

An objective examination of the whole electricity industry and the effect of the reforms leads to some interesting conclusions.

Cross subsidies

Before the reforms many power boards cross subsidised residential consumers by overcharging commercial and industrial consumers. The removal of these subsidies is a factor in the increased residential prices.

The market

The Wholesale Market Electricity Development Group made a mistake when they rejected the recommended market model and chose a market that pays all generators the price bid by the most expensive generator selected to run. This would have been a good choice if New Zealand relied entirely on fossil fuel generation. New fossil fuel power stations produce cheaper power than older ones so such a market encourages the construction of new and better stations.

In New Zealand, the cheapest generation comes from old, low cost, depreciated hydro stations. The choice of a fossil fuel market structure pays these stations the much higher price needed by the most expensive fossil fuel station. Hydro stations then rack up their asset values to camouflage the fact that they are making windfall profits

The recommended market model would have ensured that consumers would have continued to get low-cost electricity from the hydro stations that they had already paid for and built new stations that would give the lowest system costs in the long run.

The chosen market structure has led to wholesale prices increasing when they should have decreased to reflect the major reductions in operation and maintenance cost that followed on from privatisation.

Control of peak demand

Before the electricity reforms all electric water heaters in New Zealand were remotely controlled by the lines companies to reduce system peak demand by more than 10%. The reforms destroyed this world leading system. Most lines companies abandoned water heater control because the reforms did not allow them to fully recover of the costs of operating, maintaining and expanding the hot water control system.

As a result of abandoning hot water control, new power stations and a $960 million 400 kV line into Auckland were needed and millions more were spent on reinforcing transmission lines and distribution systems. All this to meet a peak demand that would not have existed with the recommended market.

Assets revalued

The reforms also allowed Transpower and lines companies to massively revalue their assets and use this increased value to justify charging consumers millions of dollars more for assets that consumers had largely paid for already. This is a major factor in the increased cost of electricity.

Traders and retailers

The electricity market also brought us traders and retailers who, it can be argued, serve no useful purpose whatsoever. The recommended market model did not need them.

In our market, traders often compete to get selected to generate. But when generation is in short supply competition is virtually non-existent and the price that they bid is “a trade-off between greed and guilt”. (On several occasions in the last few weeks wholesale prices have spiked to more than 10 times the normal price for no apparent reason.) As two retiring CEOs pointed out, the way to make money in the New Zealand market is to keep the system on the edge of a shortage. With the recommended market the system operator would have ensured that sufficient generating capacity was available and selected the generators that would give a reliable supply at the lowest cost.

Retailers increase consumer costs by spending millions of dollars trying to steal consumers from each other and pretending to compete in selling a commodity that is identical for everyone.

Conclusion

So what of the future? It does not look good. Transpower has warned that the risk of serious shortages and high prices in a dry year is rapidly increasing and no one has plans for new power stations that would mitigate this risk.

The government ignores dry year risk because it is hellbent on shutting Huntly down and limiting gas supplies and believes that exploiting wind and solar power will solve all the problems. Never mind that they are much more expensive, require backup when the wind doesn’t blow or the sun doesn’t shine and don’t make any useful contribution to meeting peak demand.

The best and cheapest way of mitigating the risk of blackouts in dry years is to ensure that Huntly continues to provide dry year reserve with two or three generating sets and 1 million tons of coal available.

The government should be taking steps to make sure that we have an economical and reliable supply into the future. If it wants to reduce CO2 – a gas that promotes plant growth and benefits our agricultural industries – it should contemplate the construction of a major and very expensive hydro pumped storage power station in the hills above Roxburgh that would solve the dry year problem. Only then can it ditch Huntly.

The New Zealand electricity market is a classic example of what happens when the politicians and the decision-makers do not understand power systems and how difficult it is to provide a reliable and economic supply. Choosing the wrong market model has cost the customer dearly.

In this exclusive series of articles by David Spratt, he explores the electric vehicle (EV) options for specific business uses.

Part 3: Evaluating the Volkswagen e-Golf electric car.

It may be that I have now test driven one too many electric vehicles (EVs), but I have become increasingly irritated by the clunky and, dare I say, ugly designs that have been rolled out by some manufacturers.

Not the e-Golf, though. Volkswagen addresses this design challenge with a vehicle that feels familiar, comfortable and accessible from the moment you climb into it. Built from the ground up to look, feel and handle like a standard Golf Super Mini, this smart town car is a delight.

I want a car that can take me safely along country roads while allowing me to travel to the city, park in tight parking spots and save money on fuel. The e-Golf ticks every one of these boxes.

It accelerates smoothly and relatively quickly (from 0 to 100kph in 9.6 seconds).

It also has, for a small car, decent boot space and plenty of leg room for front and back seat passengers. I am six feet tall (1.83 metres for those of you living in the 21st century) and found the front and rear seating gave me plenty of leg room and riding comfort. My wife, a not-so-tall person, had an issue with seeing over the steering wheel for a clear view of the road ahead. But a simple height adjustment for the seat would have addressed this issue.

I live in the rural outskirts of Auckland and so want a car that can take me safely along country roads while allowing me to travel to the city, park in tight parking spots and save money on fuel. The Volkswagen e-Golf ticks every one of these boxes.

If I was to be critical though, there were occasions when the car’s electronics got themselves into a bit of a twist and just stopped working. On at least two occasions, the parking brake and the auto hold feature for hill starts went to war, leaving me stuck in one place with a warning light and screeching sound, raising my anxiety levels. In the end, the only answer seemed to be to switch everything off and start again: fine if you are in a parking lot but not great if you are pulling out into traffic. This may be the result of an idiot behind the wheel rather than a fault, but it happened to both me and my wife on separate occasions.

Are we there yet?

Range anxiety was also an issue with the e-Golf’s distance calculator.

One moment my predicted range was displayed as 157km, then a few minutes later was 140km, only to return to 150km a while after that. I put this down to the range calculator being very sensitive to driving style and conditions, but a bit less variability would have had me more focussed on the road and less on worry about getting home on the available charge.

But charging was a breeze. At home, using a simple three-pin connector, a total recharge took around 11 hours. My favourite, free, fast charger at Counties Power HQ took 45 minutes to get me up to 80 percent, plenty of time for a coffee and a quick browse around the shops nearby.

As is the case with all the electric vehicles I have tested, the e-Golf saw me spending less than $20 per week on charging with no concessions to convenience.

Despite the car’s price of $65,990 the economics for the average business owner almost make sense. Give it a year or two and EVs like this will be a no-brainer for many business applications.

My contacts tell me the Volkswagen e-Golf is rapidly becoming a European sensation, and the future of VW motoring. I can see why. This car is a little beauty.

I gave the Volkswagen e-Golf an admiring 7.5 out of 10.

Thanks to VW New Zealand for supplying the e-Golf for testing.

Most of our electricity is provided via South Island lakes. Lake water has remained at average levels for the time of year right through the summer period thus far. What has driven the price escalations is thermal outages. A large chunk of North Island thermal generation plant has been unavailable due to maintenance.

Most of our electricity is provided via South Island lakes. Lake water has remained at average levels for the time of year right through the summer period thus far. What has driven the price escalations is thermal outages. A large chunk of North Island thermal generation plant has been unavailable due to maintenance.