New Zealand’s gas market is entering a period of structural change. PwC’s 2026 Gas Supply and Demand Study, prepared for the Gas Industry Company, highlights a future where indigenous gas supply continues to decline, major fields reach end‑of‑life, and commercial and industrial (C&I) customers face increasing uncertainty.

For businesses that rely on gas for process heat, manufacturing, food production, or backup generation, the implications are significant — and planning ahead is essential.

The State of the Gas Market: Key Findings from the PwC Study

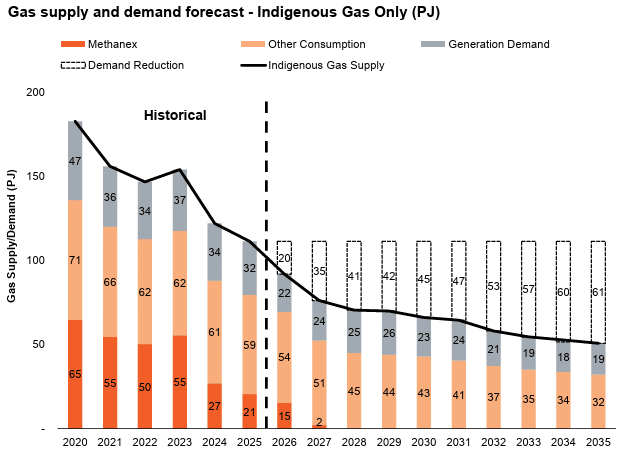

1. Domestic gas supply is declining faster than expected

New Zealand’s indigenous gas production has fallen to levels not seen in decades. Major fields are maturing, and by 2035 domestic supply could halve again. This creates structural scarcity and increases exposure to supply shocks.

2. Without LNG, the market becomes extremely tight

- Gas demand must fall sharply by 2035

- Industrial users face potential forced fuel switching

- Gas‑fired electricity generation becomes constrained

- Electricity prices become more volatile, especially in dry years

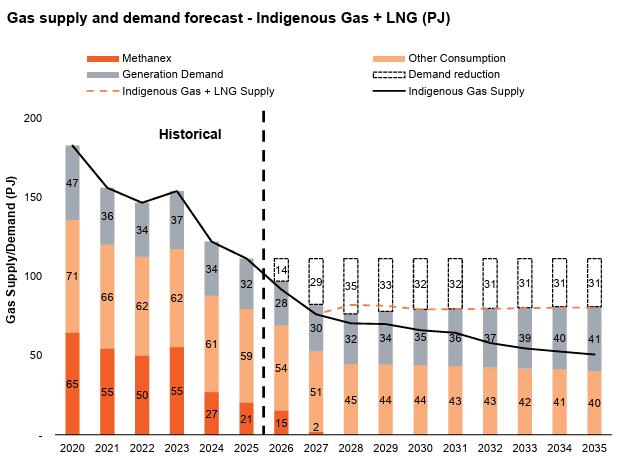

3. LNG imports from 2028 improve stability — but don’t eliminate risk

If LNG is introduced:

- Prices become more stable

- Electricity security improves

- Industrial operations remain more viable

However, LNG still exposes New Zealand to global commodity markets, and the study makes it clear that significant electrification or alternative fuels will still be required from the late 2020s onward.

4. The 2030s will be a crunch period

Even with LNG, domestic supply continues to decline. Any delays in LNG infrastructure or new supply sources increase risk for C&I customers.

What This Means for Commercial & Industrial Energy Users

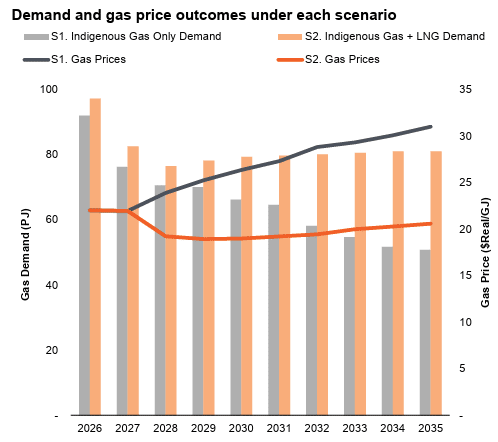

1. Expect higher and more volatile gas prices

Tight supply and declining production create upward pressure on pricing. Dry years will amplify volatility.

2. Contract availability will shrink

Retailers may:

- Shorten pricing validity windows

- Reduce willingness to quote

- Prioritise large or strategic customers

- Require longer‑term commitments

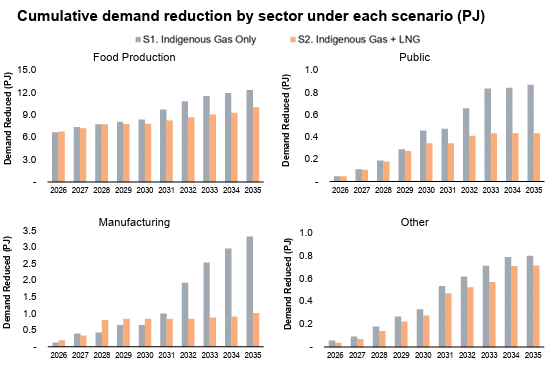

3. Forced switching is a real possibility

Industries relying on gas for process heat may face:

- Mandatory curtailment

- Loss of supply if fields decline faster than forecast

- Higher costs if switching is unplanned

4. Decarbonisation pressure will intensify

Even with LNG, the study is clear: New Zealand must electrify or adopt alternative fuels at scale.

Key Recommendations for Total Utilities Clients

1. Secure long‑term gas contracts where possible

For businesses that must remain on gas in the medium term:

- Lock in multi‑year supply agreements

- Prioritise retailers with strong upstream positions

- Consider hedging strategies

- Avoid exposure to short‑term or spot‑driven pricing

2. Begin evaluating alternative fuels now

Depending on your process heat requirements, viable options include:

- Electric boilers or industrial heat pumps

- Biomass or wood pellets

- Renewable LPG or bio‑LPG

- Hydrogen‑ready equipment

- Thermal storage solutions

3. Stress‑test your energy strategy

Consider:

- What happens if gas supply is curtailed for 30–90 days

- The impact of a dry‑year price spike

- The risk of a retailer declining to renew your contract

- The cost difference between proactive vs reactive fuel switching

4. Integrate energy security into long‑term planning

Businesses should incorporate:

- Scenario modelling

- Capex planning for alternative fuels

- Electrification roadmaps

- Carbon reduction pathways

- Contingency planning for supply interruptions

How Total Utilities Can Help

1. Gas procurement and long‑term contract negotiation

We work with all major gas supplies, helping you secure competitive, reliable supply in a tightening market. Over the last few months we have been securing contracts of up to 5 years and while this does not guarantee gas supply, it does provide long term gas pricing security.

2. Ongoing market intelligence

We continuously monitor:

- Gas supply conditions

- Retailer behaviour

- LNG developments

- Electricity market dynamics

- Policy and regulatory changes

3. Decarbonisation and feasibility studies

Our technical partners can assist your business build practical, staged plans that balance cost, operational requirements, carbon reduction, technology readiness, and risk management. From engineering assessments to procurement and implementation, they guide you through the entire transition process.

Final Thoughts

The PwC study is a clear signal: New Zealand’s gas market is tightening, and C&I customers must prepare for a future where gas is more expensive, less available, and increasingly uncertain.

Whether your business intends to stay on gas for the medium term or transition away from it, the decisions you make in the next 12–24 months will shape your resilience and competitiveness through the 2030s.

Total Utilities is here to help you navigate that journey with clarity, confidence, and data‑driven strategy.