The Current State of Affairs and the Impact of Deferred Investments

Well, not that much sadly, but the optimist in me sees green shoots of regulatory progress, some generation development activity (at last), but a continued chorus of gas concerns from the choir of Generator/Retailers (gentailers) who benefit hugely from fossil fuel generation being the margin, price setting unit for spot prices.

Of course, mother nature plays her hand in New Zealand Electricity prices, increasingly so as we live with the outcome of deferred investment in new generation and the low level of attractiveness of New Zealand for new investment due to the market power exercised by a largely state owned incumbent generation sector.

Well, there have been some announcements that might ordinarily be cause for optimism; the formation of the Energy Competition Taskforce which brought together the three historically benign regulators in the Electricity Authority, the Commerce Commission and MBIE to address the mounting (mountain?) of evidence that New Zealand Electricity market isn’t delivering the outcomes we would expect for a nation so well-endowed in natural energy resources.

To their credit the task force has already implemented changes that might help, albeit at the margin with developments like adding super peak prices to the ASX energy futures market which has seen some improved liquidity and price disclosure across super peak products, and perhaps a lower peak/off-peak differential in pricing, though this may be more a reflection of increased fossil fuel pricing in off-peak periods. IE higher overall prices.

The task force has also announced a consultation on several potentially significant changes grouped as “level playing field measures”. The “proposed nondiscrimination obligations” would require Gentailers not to treat themselves substantially differently from their non-integrated competitors, or to treat different competitors substantially differently. Given the openness with which the vertically integrated incumbents have posted losses on retail while making record overall profits over the last few years this seems blindingly obvious, as a measure. It would see gentailers having to build a portfolio of internal transfer prices for hedges which would make it far more transparent for the regulators to assess hedge access (market power) issues.

Should this measure still not result in the market delivering competitive outcomes, a second measure sits behind this as a backstop, he proposed “virtual disaggregation measures” refers to splitting the flexible generation capacity of participants who exceed a certain market share into two components: a portion that would be required to be offered, and a portion that would be used by the participant as they see fit.

The Role of Government Dividends

It remains to be seen the extent to which the task force resists the inevitable strong lobbying against these measures from the incumbent players and if implemented how long it takes before we see a return to meaningful retail competition and real customer innovation.

My bet is that we will see all sorts of ballyhoo from the incumbents about how hard they are doing great, and of course, the elephant in the room is the dividends received by the government from their state-controlled gentailers, Genesis, Meridian and Mercury. I’m yet to see an economic analysis to support any assertion that the value of those dividends outweighs the value to our economy of cheap abundant energy delivered through an undistorted or workable efficient market….

However, the Q4 2024 MBIE Energy consumption Stats show that the current market isn’t working for Kiwi businesses with a 9% year-on-year fall in electricity demand from the industrial sector.

Some of this will no doubt be the closure of Winstone Pulp International and the Oji Fibre Solutions’ Penrose plants citing energy cost as a major factor in those decisions, and part is also likely the ramp down of Tiwai at Meridian’s request.

There was much heralding of the benefits to New Zealand of the new Tiwai deal, especially by Meridian:

“This is a fantastic outcome for New Zealand and the Southland region. It’s further proof that large industrial businesses can utilise New Zealand’s renewable energy advantage and create low carbon sustainable products, high value jobs and export dollars for our country.”

But now it would seem that it’s even better for New Zealand when Tiwai doesn’t run. Curious that!

Future Outlook

Another winter of extreme prices in 2025 poses yet another threat to consumer confidence in New Zealand’s electricity market, ultimately threatening the social license that incumbent generators and even distribution businesses have enjoyed for so long.

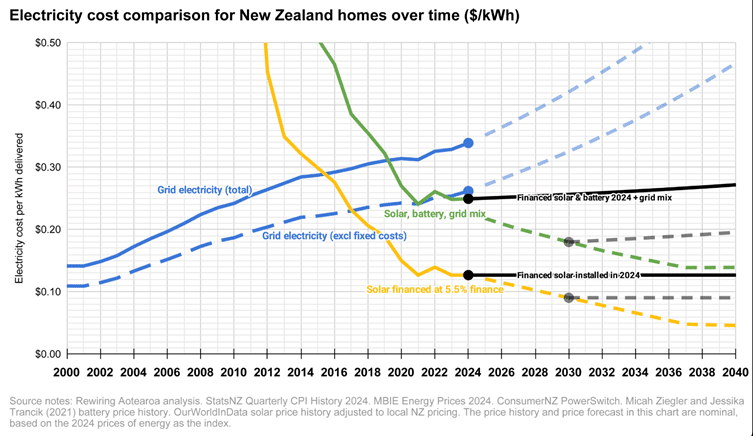

The reality is that in 2025, for perhaps the first time, grid supply companies may be facing the legitimate threat of substitution as New Zealand’s (and global) grid energy supply becomes more expensive than the delivered cost of rooftop solar for residential consumers.

Recommendations for Businesses

The same trends apply to supply for business consumers, I would go so far as to say that any business in New Zealand facing new supply costs should feel obliged to seek a quote on rooftop solar and battery.

The economics of rooftop solar in terms of delivered cost of energy will continue to improve as regulatory reforms evolve to incentivise consumers to participate in flexibility, and reward investment in distributed energy resources. While escalating grid and distribution costs are now locked in for the next five-year period we should expect to see this continue to increase. From a global perspective, New Zealand is no different to most nations looking to electrify their economies. According to Bloomberg New Energy Finance research, US$21 trillion dollars of grid investment is required to reach net zero emissions targets.

We can expect to see more and more businesses taking their destiny into their own hands as our incumbent grid suppliers seek to maximise returns from legacy assets against the improving economics of generation technologies that can generate energy at the point of consumption.

If 2024 taught us anything, it’s that unpredictability is the new norm. From gas shortages and hydro lake levels nearing rock bottom to record highs and lows in pricing, the year had it all.

One thing is clear: the current market structure isn’t serving commercial and industrial customers well. Short-term issues have impacted long-term pricing, forcing customers to pay a premium for future energy, even when conditions might improve.

In a previous article, I delved deeper into how coal sets the overall price in a largely renewable energy grid. You can read more about it here.

Looking Ahead to 2025

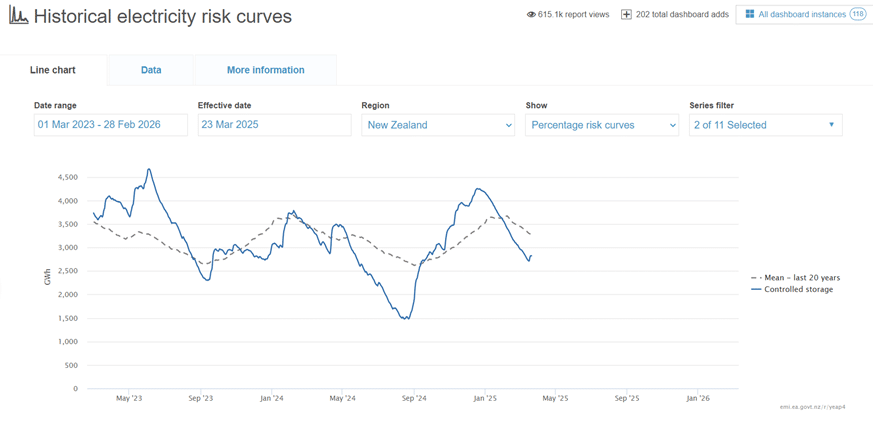

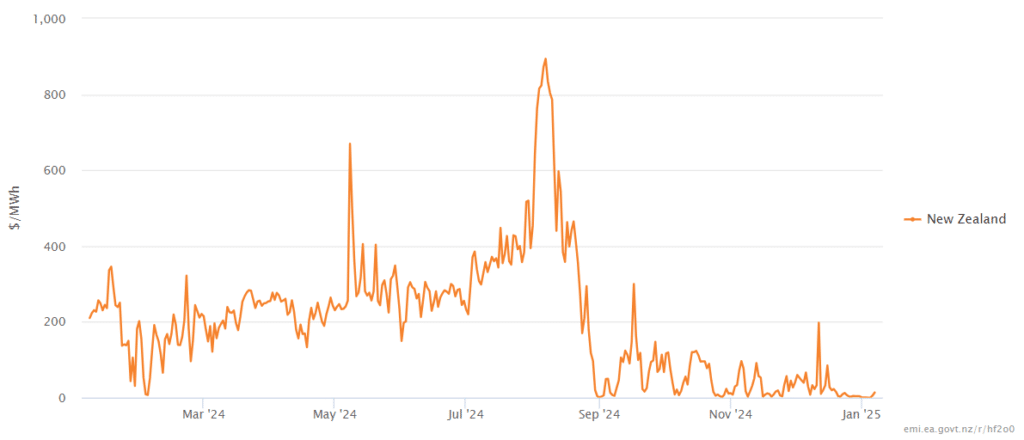

As we step into 2025, hydro storage levels are at 85% capacity, which is 22% higher than usual for this time of year. Wholesale electricity spot pricing remains low, with thermal generation contributing only about 3-5% to the grid. Current prices are around 4-5c/kWh, a significant drop from last January’s 25c/kWh. However, with limited natural gas availability and coal firming the market, price volatility is more pronounced, especially during dry periods when wind generation drops.

Average Daily Wholesale Spot Pricing

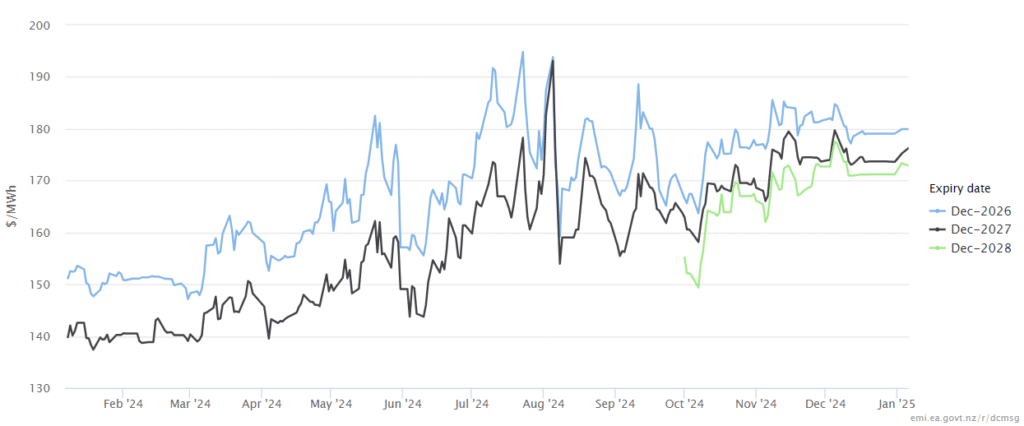

The ASX Energy Futures Market

Forward market pricing remains stubbornly high on the ASX Energy Futures market, which sets the overall forward price for retail contracts for large commercial and industrial customers. The current quarter (Jan-Mar 2025) is priced around 12c/kWh in the North Island and 7.4c/kWh in the South Island.

The ASX Energy Futures market is dominated by the big four generators: Contact, Genesis, Mercury, and Meridian. These generators offer volume into the market for participants, which can include other generators, retailers, major energy users, or investment houses.

Long-Term Pricing Trends

Over the past year, long-term pricing on the ASX has steadily increased as natural gas supplies dwindle. The market seems to be factoring in more risk as coal becomes the dominant fuel for managing limited hydro storage.

North Island pricing for 2026, 2027, and 2028 has risen by 19%, 26%, and 11% respectively since January last year. Similarly, South Island prices have increased by 28%, 35%, and 14%. Notably, pricing for 2028 only became available on the market from October 1st last year. The forward price curve has also shifted from a staggered reducing price to an almost flat price within any given year.

North Island Pricing ASX Energy Futures

The Future of Firming Fuels

This trend suggests that coal will remain the firming fuel of choice for the foreseeable future, despite calls for liquid natural gas imports as a lower carbon emission option. The industry appears divided on future firming solutions, adding to the uncertainty.

As we navigate through 2025, staying informed and adaptable will be key to managing the ever-changing energy landscape.

Navigating the Future of Renewable Energy and Market Volatility

The announcement of new renewable generation projects is exciting, but it comes with its own set of challenges. Much of the new capacity is in solar and wind, both of which are intermittent and cannot be relied upon for firming. While battery storage is becoming more economically viable, it hasn’t reached the point where it can fully replace traditional firming methods. New hydro or geothermal developments, which could provide the necessary baseload generation to support intermittent sources, are facing lower priority due to high costs and resource consent issues.

What to Expect in the Coming Year

As we look ahead, the energy market is expected to remain volatile. Both Transpower and the Gas Industry Company have warned that natural gas production may fall below demand during the upcoming winter. This shortfall will likely keep energy prices unstable. Additionally, the commissioning of new generation projects is progressing slowly, meaning the reliance on fossil fuels for firming will continue in the short term.

Preparing for Contract Expiry in 2025

If your electricity contract is set to expire in 2025, it’s crucial to start planning early. Seeking market pricing well in advance of your contract’s expiry date allows you to set realistic budgets and mitigate the impact of short-term volatility.

Consider exploring solar options, whether on-site or off-site. Both approaches enable you to purchase solar energy as a commodity, reducing your exposure to price fluctuations in the broader energy market.

How Total Utilities Can Help

Total Utilities is here to assist you in navigating these complexities. We offer advisory services to help you evaluate your options and make informed decisions about your energy contracts and renewable energy investments. For more detailed advice, you can read our article on managing utility contract expirations here.

By staying proactive and informed, you can better manage the uncertainties of the energy market and make strategic decisions for your business’s future.

Changes to national grid operator Transpower’s transmission charges took effect in April – and as with most things in life, there are winners and losers.The updated transmission pricing methodology (known as TPM) significantly differs from previous years, and has delivered a mixed bag of rises and cuts for domestic and industrial users.

State owned enterprise, Transpower, has been allowed to recover $830 million by the Commerce Commission for running the network and the increased costs are now being passed on to end users.

Changes to charging methodology

Transpower Head of Grid Pricing Rebecca Osborne said the Electricity Authority has designed the new methodology to more closely reflect the costs and expected benefits of electricity transported across Transpower’s 12,000 kilometres of transmission lines.

There should be no surprises across the electricity industry about the new transmission charges, she said.

“We’ve consulted with customers along the way and provided information as the elements have developed, including updating our indicative prices… and providing indicative rates information in early November.”

“Total transmission revenue, as set by the Commerce Commission, remains the same, but how it is distributed among Transpower customers has changed.”

Encourage renewable generation

The Authority expects the new approach to transmission charges to encourage investment in renewable generation and electrification of industrial processes.

According to Transpower, the main change in the new transmission pricing is a move to a benefit-based approach where customers pay in proportion to the benefit they are expected to receive from some historic and all future transmission investments.

The previous methodology spread the cost of the HVDC (High Voltage Direct Current) link connecting the two main islands across South Island generators and spread the cost of all other interconnection assets across local lines companies and major industrial users.

Some Northland, East & West Coast customers hit hardest

In general, this means cost increases for local lines companies and some of the largest industrial customers in the north of the country because they are further away from where the bulk of generation is located in the South Island.

It also means North Island generators will begin contributing to the cost of the interconnected transmission assets and South Island generators will contribute less.

Consumers in Northland, the east coast of the North Island, and the West Coast have faced the biggest hikes, while Wellington and some South Island areas have seen prices fall.

The final amount that consumers pay for their transmission charges is ultimately decided by local lines companies, these charges typically make up between 8 and 10 percent of power bills.

Big power users such as the Tiwai Point aluminium smelter have seen an almost $10m price cut, while NZ Steel mill at Glenbrook faces an $11m increase.

Earlier in the year the Electricity Authority calculated movements would generally be small.

Those most affected may take issue with this. Indeed, Buller Electricity filed for a judicial review after being told its transmission charges would rise by 427 percent.

Total Utilities is New Zealand’s largest issuer of business-to-business energy procurement tenders, providing energy purchasing services to many household names. With around 500 tenders issued to the market every year, getting favourable terms is crucial. But negotiating energy contracts is so much more than getting a great price. It involves an understanding of the many moving parts.

The variables that influence retail energy prices are:

GEOGRAPHICAL

New Zealand’s population is dispersed over a large land area, creating its own set of challenges.

FINANCIAL

Prices are based on the changing supply and demand through the wholesale spot market.

MARKET-DRIVEN

The market is deregulated, and our national energy supply consists of generators/retailers, the national grid operator and 29 local distribution companies. Energy retailers can hedge future energy on the ASX Energy Futures market.

SOURCE OF ENERGY

New Zealand has a diverse generation fleet, including hydro, geothermal, wind, and coal.

REGULATORY

The Emissions Trading Scheme, Net Zero 2050 and shifting government policy influence generator behaviours.

TIMING

Changes to hydro storage and government policy mean windows of opportunity can be very limited in the energy market.

That’s why engaging independent energy consultants who understand the variables, the available options and when to time procurement events is so worthwhile.

Let’s look at different scenarios where our clients saved significant sums because they had Total Utilities on their side.

TIMING MATTERS Leaving a negotiation too late gives retailers an unfair advantage, as customers have limited options to choose from. A large university’s contract was due to expire, and they were concerned about going to market too soon. They usually would wait until two or three months before expiry to begin researching options. However, we encouraged them to procure their contract with eight months to go. In doing so, they avoided a 36% cost increase and saved over $2 million.

WE ARE LEVERAGING COMPETITIVE TENSION: A national food producer was given a renewal offer from their energy supplier and told that this was the most competitive option in the market.At Total Utilities, though, we understand that retailers don’t always put their best foot forward unless you give them a push. After we went through a competitive tender process, we negotiated a new renewal offer of over $500,000 less than the previous offer.

DOWNGRADING YOUR METER CAN MAKE A DRAMATIC DIFFERENCE An Auckland-based packaging customer was facing a 40% cost increase over three years. Their retailer was only giving them pricing based on their current meter configuration. This is typical in New Zealand because, unlike other countries, there isn’t a fully contestable meter supplier market. Despite being a large commercial customer, they could downgrade their meter because of their connection size. Total Utilities helped with the meter downgrade and negotiated new pricing on their behalf. As a result, they reduced their cost increase by 75% over three years and saved $200,000. The customer couldn’t believe that changing their meter would have such an impact on their new contract prices.

WE ARE ACTING QUICKLY TO HELP CLIENTS IN NEED A Christchurch-based supplier and manufacturer of commercial refrigeration equipment had been out of contract for more than two months. Struggling on their own to get offers for energy supply, they were at risk of costly spot pricing. Spot pricing changes every half hour making it a volatile and expensive route. The customer asked us for help after getting a renewal offer from their current supplier. The trouble was the offer represented a whopping 225% increase over the next 12 months.Within just five days, we presented the customer with our recommendations. We laid out several energy supply options with different retailers. The best option was 150% lower over the first 12 months than the one previous. What’s more, the new contract was backdated over two months. This meant they avoided default spot prices. Overall, the best option was 27% more cost-competitive over the term of the agreement.

The right energy procurement is crucial

Total Utilities are so much more than negotiators. We have a deep and long-term understanding of the energy market and the many factors that influence supply, price, and demand.You don’t have to settle for the first offer on the table. By engaging us, we leverage the right timing and competitive tension to get you the most favourable terms, saving you significant sums of money over the duration of your contract.