After winter 2024 saw spot prices exceed $800/MWh resulting in unprecedented Ministerial scrutiny on regulators (“chocolate teapots” according to Associate Energy Minister Hon. Shane Jones), businesses leaving New Zealand altogether citing unsustainable energy costs, the question now is…. What’s changed?

The Current State of Affairs and the Impact of Deferred Investments

Well, not that much sadly, but the optimist in me sees green shoots of regulatory progress, some generation development activity (at last), but a continued chorus of gas concerns from the choir of Generator/Retailers (gentailers) who benefit hugely from fossil fuel generation being the margin, price setting unit for spot prices.

Of course, mother nature plays her hand in New Zealand Electricity prices, increasingly so as we live with the outcome of deferred investment in new generation and the low level of attractiveness of New Zealand for new investment due to the market power exercised by a largely state owned incumbent generation sector.

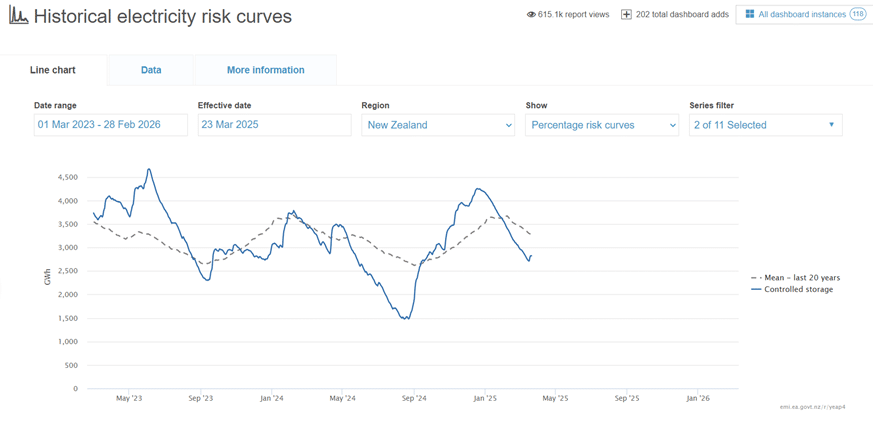

As it stands at the time of writing (21/03/20205) New Zealand is sitting on 2822 GWh of storage, by comparison, on the same day in 2024 storage was at 3149GWh of storage.

Source: EMI 21/03/2025

Regulatory Developments and Taskforce Initiatives

So, Groundhog Day you say?

Well, there have been some announcements that might ordinarily be cause for optimism; the formation of the Energy Competition Taskforce which brought together the three historically benign regulators in the Electricity Authority, the Commerce Commission and MBIE to address the mounting (mountain?) of evidence that New Zealand Electricity market isn’t delivering the outcomes we would expect for a nation so well-endowed in natural energy resources.

I personally don’t think that it’s a coincidence that the group included the Com Com after a number of independent electricity retailers laid complaints to the Commerce Commission alleging breaches of the new enhanced market power provisions of Section 36 of the Commerce Act.

To their credit the task force has already implemented changes that might help, albeit at the margin with developments like adding super peak prices to the ASX energy futures market which has seen some improved liquidity and price disclosure across super peak products, and perhaps a lower peak/off-peak differential in pricing, though this may be more a reflection of increased fossil fuel pricing in off-peak periods. IE higher overall prices.

The task force has also announced a consultation on several potentially significant changes grouped as “level playing field measures”. The “proposed nondiscrimination obligations” would require Gentailers not to treat themselves substantially differently from their non-integrated competitors, or to treat different competitors substantially differently. Given the openness with which the vertically integrated incumbents have posted losses on retail while making record overall profits over the last few years this seems blindingly obvious, as a measure. It would see gentailers having to build a portfolio of internal transfer prices for hedges which would make it far more transparent for the regulators to assess hedge access (market power) issues.

Should this measure still not result in the market delivering competitive outcomes, a second measure sits behind this as a backstop, he proposed “virtual disaggregation measures” refers to splitting the flexible generation capacity of participants who exceed a certain market share into two components: a portion that would be required to be offered, and a portion that would be used by the participant as they see fit.

The Role of Government Dividends

It remains to be seen the extent to which the task force resists the inevitable strong lobbying against these measures from the incumbent players and if implemented how long it takes before we see a return to meaningful retail competition and real customer innovation.

My bet is that we will see all sorts of ballyhoo from the incumbents about how hard they are doing great, and of course, the elephant in the room is the dividends received by the government from their state-controlled gentailers, Genesis, Meridian and Mercury. I’m yet to see an economic analysis to support any assertion that the value of those dividends outweighs the value to our economy of cheap abundant energy delivered through an undistorted or workable efficient market….

However, the Q4 2024 MBIE Energy consumption Stats show that the current market isn’t working for Kiwi businesses with a 9% year-on-year fall in electricity demand from the industrial sector.

Some of this will no doubt be the closure of Winstone Pulp International and the Oji Fibre Solutions’ Penrose plants citing energy cost as a major factor in those decisions, and part is also likely the ramp down of Tiwai at Meridian’s request.

There was much heralding of the benefits to New Zealand of the new Tiwai deal, especially by Meridian:

“Meridian Energy chief executive Neal Barclay called the agreement an “excellent result” after many years of negotiation.

“This is a fantastic outcome for New Zealand and the Southland region. It’s further proof that large industrial businesses can utilise New Zealand’s renewable energy advantage and create low carbon sustainable products, high value jobs and export dollars for our country.”

But now it would seem that it’s even better for New Zealand when Tiwai doesn’t run. Curious that!

Future Outlook

Another winter of extreme prices in 2025 poses yet another threat to consumer confidence in New Zealand’s electricity market, ultimately threatening the social license that incumbent generators and even distribution businesses have enjoyed for so long.

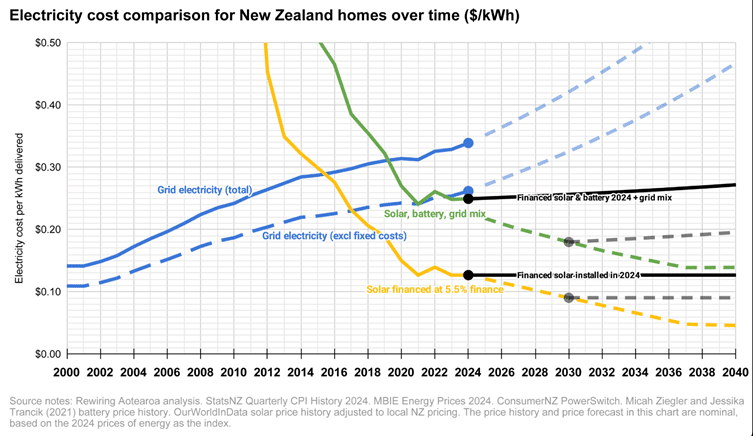

The reality is that in 2025, for perhaps the first time, grid supply companies may be facing the legitimate threat of substitution as New Zealand’s (and global) grid energy supply becomes more expensive than the delivered cost of rooftop solar for residential consumers.

Recommendations for Businesses

The same trends apply to supply for business consumers, I would go so far as to say that any business in New Zealand facing new supply costs should feel obliged to seek a quote on rooftop solar and battery.

The economics of rooftop solar in terms of delivered cost of energy will continue to improve as regulatory reforms evolve to incentivise consumers to participate in flexibility, and reward investment in distributed energy resources. While escalating grid and distribution costs are now locked in for the next five-year period we should expect to see this continue to increase. From a global perspective, New Zealand is no different to most nations looking to electrify their economies. According to Bloomberg New Energy Finance research, US$21 trillion dollars of grid investment is required to reach net zero emissions targets.

We can expect to see more and more businesses taking their destiny into their own hands as our incumbent grid suppliers seek to maximise returns from legacy assets against the improving economics of generation technologies that can generate energy at the point of consumption.